Executive Summary & Analyst Perspective

India's Battery Energy Storage Systems (BESS) market is no longer nascent – it is accelerating. After years of policy deliberation, pilot projects, and cautious capital deployment, 2024‑25 marks a structural inflection point. The confluence of ambitious renewable‑energy targets (500 GW by 2030), a deteriorating grid‑stability outlook, rapidly falling lithium‑ion prices, and bold government procurement signals has created conditions for explosive BESS deployment across every market segment.

At Eninrac, we track energy‑transition markets with granular data intelligence. Our assessment is unambiguous: India’s BESS market is entering its tipping point. The question is no longer “if” – it is “who captures this opportunity first.” This report dissects the opportunity across four critical segments: Front‑of‑the‑Meter (FTM), Behind‑the‑Meter (BTM), Commercial & Industrial (C&I), and DISCOM‑anchored deployments.

Global BESS Market – Setting the Stage

Global Market Overview

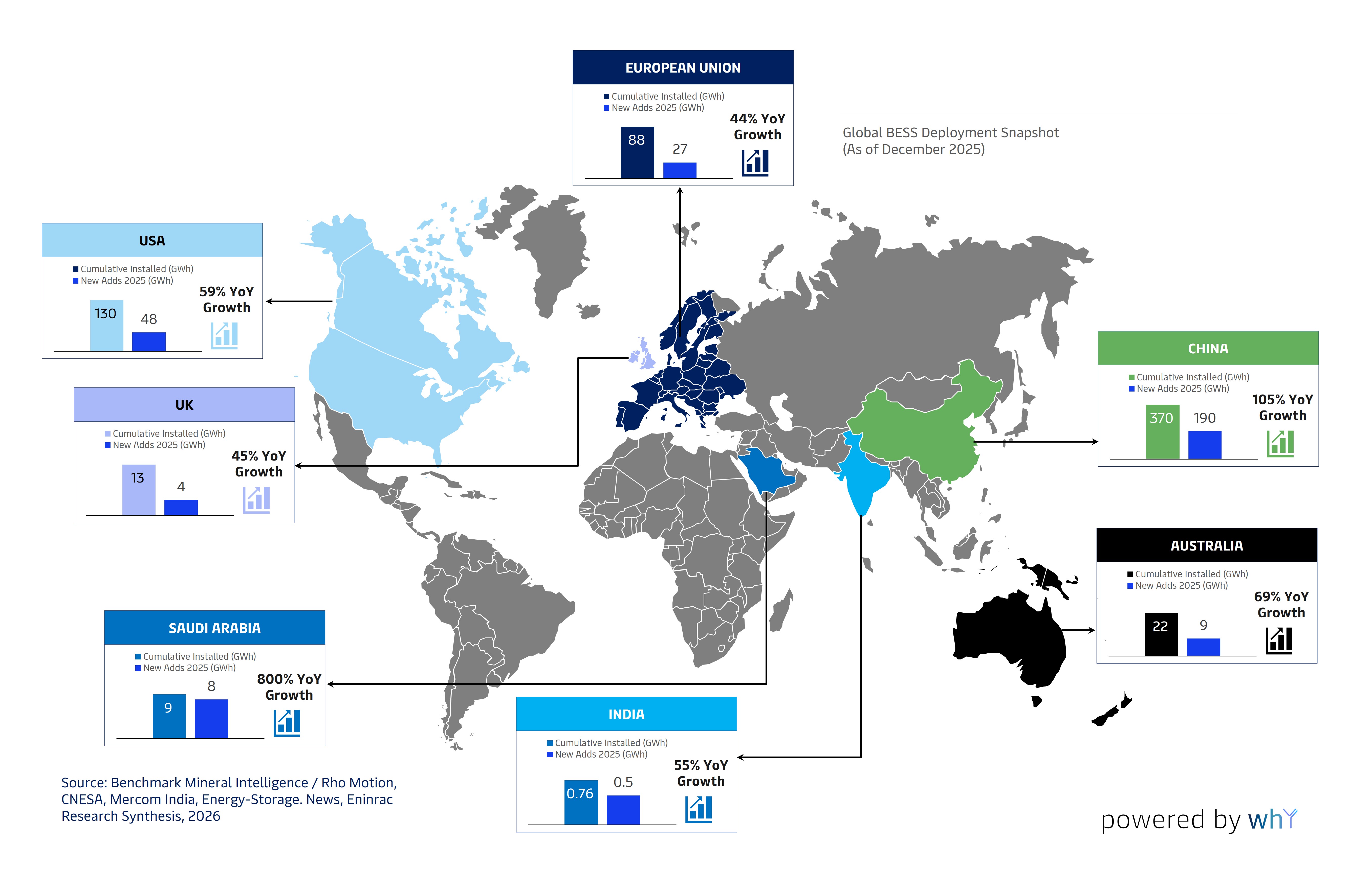

The global BESS market crossed a landmark 615 GWh of cumulative installed capacity in 2025, with annual new additions of approximately 315 GWh which represents nearly 50% year-on-year growth over 2024. China and the United States continued to lead deployments, with China's dominance reaching extraordinary proportions: in December 2025 alone, China installed more battery storage capacity than the US deployed across the entire year. Meanwhile, the rest of the world experienced a staggering 242% jump in deployments, highlighting rapid acceleration of BESS adoption outside the traditional major markets. Yet India's story may be the most consequential of all, since the total pipeline of BESS projects stands at 92 GWh in India, increasing by 74 GWh from just 19 GWh in 2024 a structural inflection that mirrors what China experienced between 2019 and 2022.

India's gap is starker than ever

India's cumulative installed energy storage capacity reached only 490 MWh by end of June 2025, and commissioning capacity for the full year stood at 0.5 GWh in 2025 - meaning India commissioned in an entire year what China installs in roughly 4 hours.

India’s pipeline explosion is real story

A total of 69 tenders accounting for 102 GWh were issued during 2025 - a 35% jump from 2024 and almost equal to the cumulative of all tenders issued from 2018 to 2024.

Cost Trajectory Update

BESS system pricing reached new lows in 2025, with project tenders in China falling to as low as $63/kWh., and battery pack prices for stationary storage fell to $70/kWh in 2025 - a 45% decrease from 2024, which is the steepest decline among all lithium-ion categories.

India at the Tipping Point – Current Market State

The Grid Reality That Is Forcing BESS

India's power sector is facing a dual stress: surging peak demand and the paradox of curtailment. Solar generation peaks mid-day when demand is moderate, yet evening peaks (6–10 PM) strain transmission infrastructure. In 2024, India experienced over 890 hours of grid stress events exceeding 175 GW demand. Meanwhile, over 2,800 MU of renewable energy was curtailed which is equivalent to powering Pune for 4 months. BESS is the structural answer to both problems simultaneously.

India – Key Metrics for BESS Market in India at a Glance (2025)

| Parameter | Current Status (2025) | 2030 Target / Trajectory |

|---|---|---|

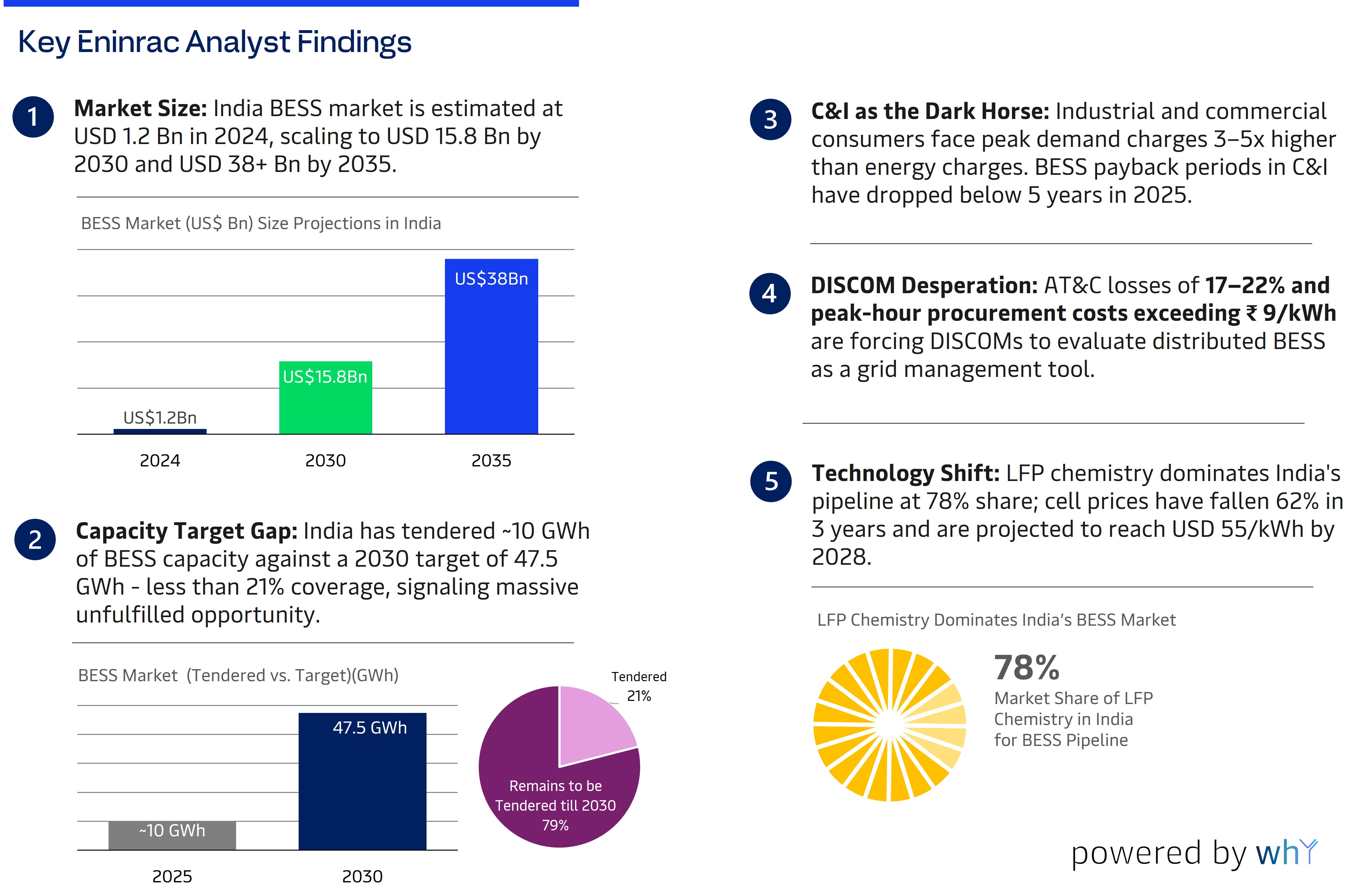

| Installed BESS Capacity | ~1.1 GWh (operational) | 47.5 GWh (National Target) |

| Tendered Capacity | ~10 GWh under various tenders | Accelerating pipeline |

| No. of Projects (>1 MW) | 34 projects commissioned | 500+ expected by 2030 |

| VGF Scheme Allocation | Rs. 9,400 Cr for Phase I (4 GWh) | Phase II & III in planning |

| Average LCOS (Grid) | Rs. 8.5–10.5/kWh | Rs. 5.5–7.0/kWh by 2030 |

| Peak Demand (2024) | 246 GW (record) | 335–360 GW by 2030 |

| RE Installed Capacity | 186 GW (Wind+Solar) | 500 GW target |

| Market Value (2024) | USD 1.2 Bn | USD 15.8 Bn by 2030 |

| Domestic Cell Manufacturing | ~0.5 GWh (PLI beneficiaries) | 50 GWh target by 2030 |

Key Policy Triggers Unlocking BESS Market in India

| Policy/Scheme | Issuing Authority | BESS Impact | Eninrac Assessment |

|---|---|---|---|

| National Energy Storage Policy | MoP, 2023 | Defines 47.5 GWh target | HIGH - Framework setter |

| VGF for BESS | MNRE / NTPC | Rs.9,400 Cr for 4 GWh Tranche 1 | CRITICAL - Demand trigger |

| PLI for ACC Batteries | MHI | 50 GWh manufacturing capacity | HIGH - Supply enabler |

| RDSS Scheme | MoP / DISCOMs | Smart metering + grid upgrade enabling BESS | MEDIUM-HIGH |

| Renewable Purchase Obligation | State SERCs | Drives RE + Storage bundling | HIGH - Market pull |

| Ancillary Services Market | CERC / NLDC | BESS can monetize as frequency provider | MEDIUM - Evolving |

| BESS Tendering (SECI/NTPC) | SECI, NTPC, State DISCOMS | Direct procurement mechanism | CRITICAL - Volume driver |

Regulatory & Policy Framework

Evolution of India's BESS Regulatory Architecture

India's regulatory approach to BESS has matured significantly since the first draft energy storage policy in 2021. The current framework now spans procurement policy, technology mandates, grid code integration, financial support mechanisms, and manufacturing incentives. What remains incomplete and where Eninrac sees the most near-term opportunity - is the ancillary services market, wheeling & banking charges for storage, and a standardized BESS lease / OPEX model framework for commercial deployments.

Regulatory Milestone Timeline – For BESS in India

| Year | Regulation / Order | Key Provision | Eninrac Impact Rating |

|---|---|---|---|

| 2017 | CERC Order on ES | First recognition of storage in grid code | ★★☆☆☆ (Foundational) |

| 2020 | MoP Draft Policy | Mandated RE+Storage integration framework | ★★★☆☆ (Directional) |

| 2022 | CERC RE+ES Regulations | Framework for hybrid RE‑BESS tariff & dispatch | ★★★★☆ (Commercial) |

| 2022 | PLI for ACC | 50 GWh manufacturing target, Rs 18,100 Cr incentive | ★★★★★ (Game‑changer) |

| 2023 | National ES Policy | 47.5 GWh BESS target; VGF mechanism announced | ★★★★★ (Market anchor) |

| 2023 | MNRE VGF Guidelines | Rs 9,400 Cr support for 4 GWh Tranche I | ★★★★★ (Demand trigger) |

| 2024 | CERC Ancillary Services | BESS eligible for primary & secondary frequency control | ★★★★☆ (Revenue model) |

| 2024 | State BESS Policies | Rajasthan, Gujarat, Maharashtra issue BESS‑specific policies | ★★★★☆ (State momentum) |

| 2025 | RDSS Phase II | Distribution upgrade unlocks smart BESS deployment | ★★★☆☆ (Enabler) |

Critical Regulatory Gaps – Eninrac Identified

- Wheeling & Banking: No uniform national policy on storing solar power and drawing it back later, creating project bankability risk. States like Rajasthan are progressive; Bihar & eastern states lag.

- BESS as a “Transmission Asset”: Classification as a regulated transmission asset (and thus, offtake guaranteed) is unsettled – critical for large FTM projects.

- GST Parity: BESS systems attract 18 % GST on components versus 5 % for pure solar, adding 6‑8 % cost. Rationalisation would reduce system cost.

- Standardised PPA Framework: Absence of a BESS‑specific PPA template delays financial closure by 6‑12 months per project. SECI has begun drafting templates.

Unlock the Full India BESS Market Report

We’ve shared a preview of the key insights. To receive the complete report (all slides, data tables, forecasts and analysis), simply click the button below, fill in a short form, and we’ll email the PDF to you instantly.