Executive Summary & Analyst Perspective

- India is poised not just to meet its domestic solar needs, but to emerge as a global supply hub by 2030

- Rising demand, geopolitical shifts, and a maturing ecosystem are creating a golden window for solar manufacturing expansion

- Solar cells and modules are at the forefront of India’s energy transition and industrial growth narrative

- Waaree Energies targets a 75% expansion in solar module manufacturing by FY27, aligning with India’s push for self-reliance

- TP Solar ramps up module capacity from 0.6 GW in Q1 FY25 to 4 GW by FY26, a nearly 7x scale-up in 5 quarters

- PLI outlay for solar manufacturing has grown over 5x since 2021, signaling India’s aggressive push for solar self-reliance

- PLI 2.0 aims to add over 40 GW of integrated solar PV capacity, bolstering India’s manufacturing independence

- India’s solar PV manufacturing is expected to grow at 18.9% CAGR (BAU), with bullish scenarios crossing 240 GW by 2030

- Strong government support via ALMM and subsidies fuels optimistic solar growth outlook (25.38% CAGR under BULL scenario)

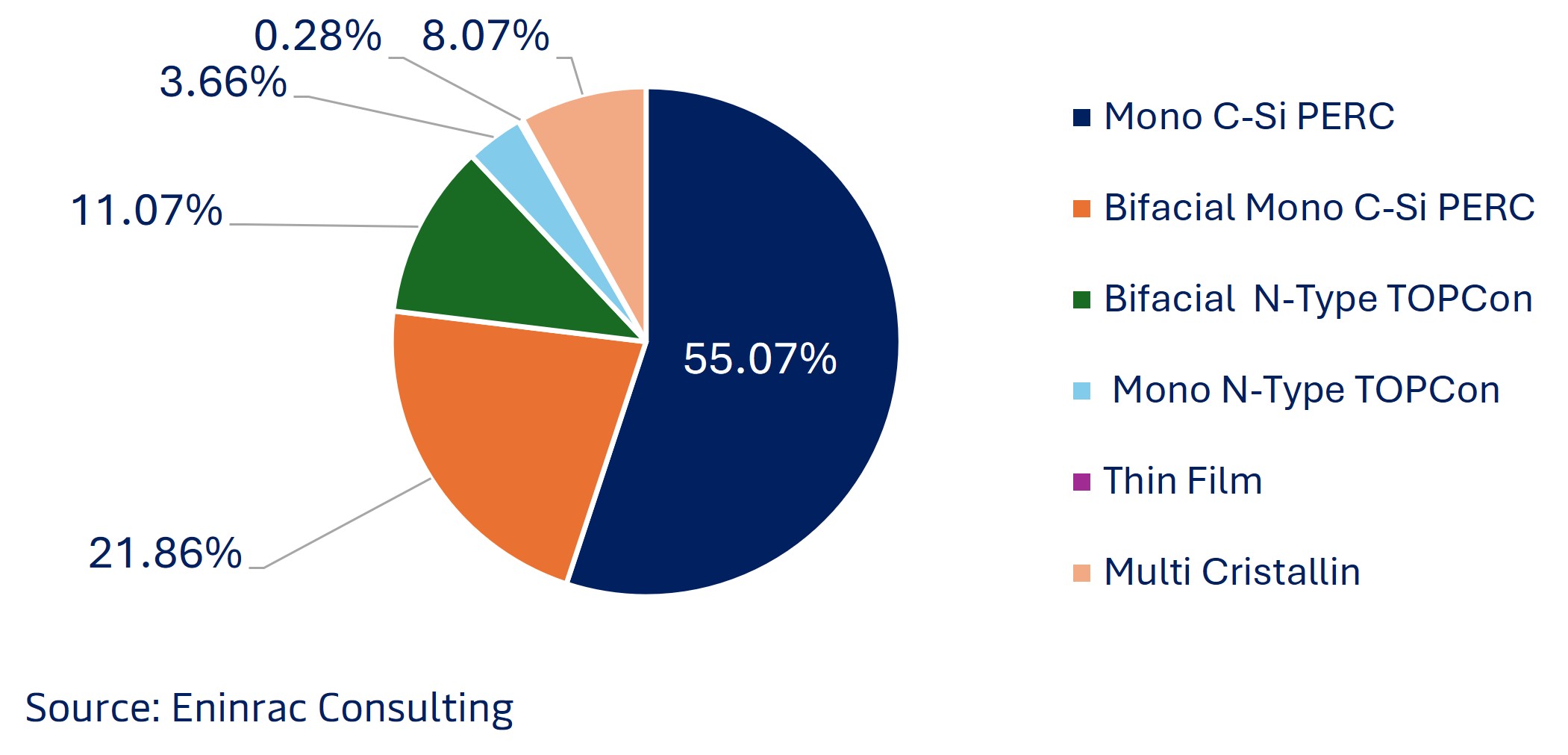

As of February 2025, Mono C-Si PERC continues to dominate the PV module market, accounting for 55.07% of the 1,066 enlisted module types. However, emerging technologies like TOPCon, particularly Mono N-Type TOPCon and Bifacial N-Type TOPCon are gaining traction, together making up over 14% of the total share, indicating a gradual shift towards higher-efficiency solutions.

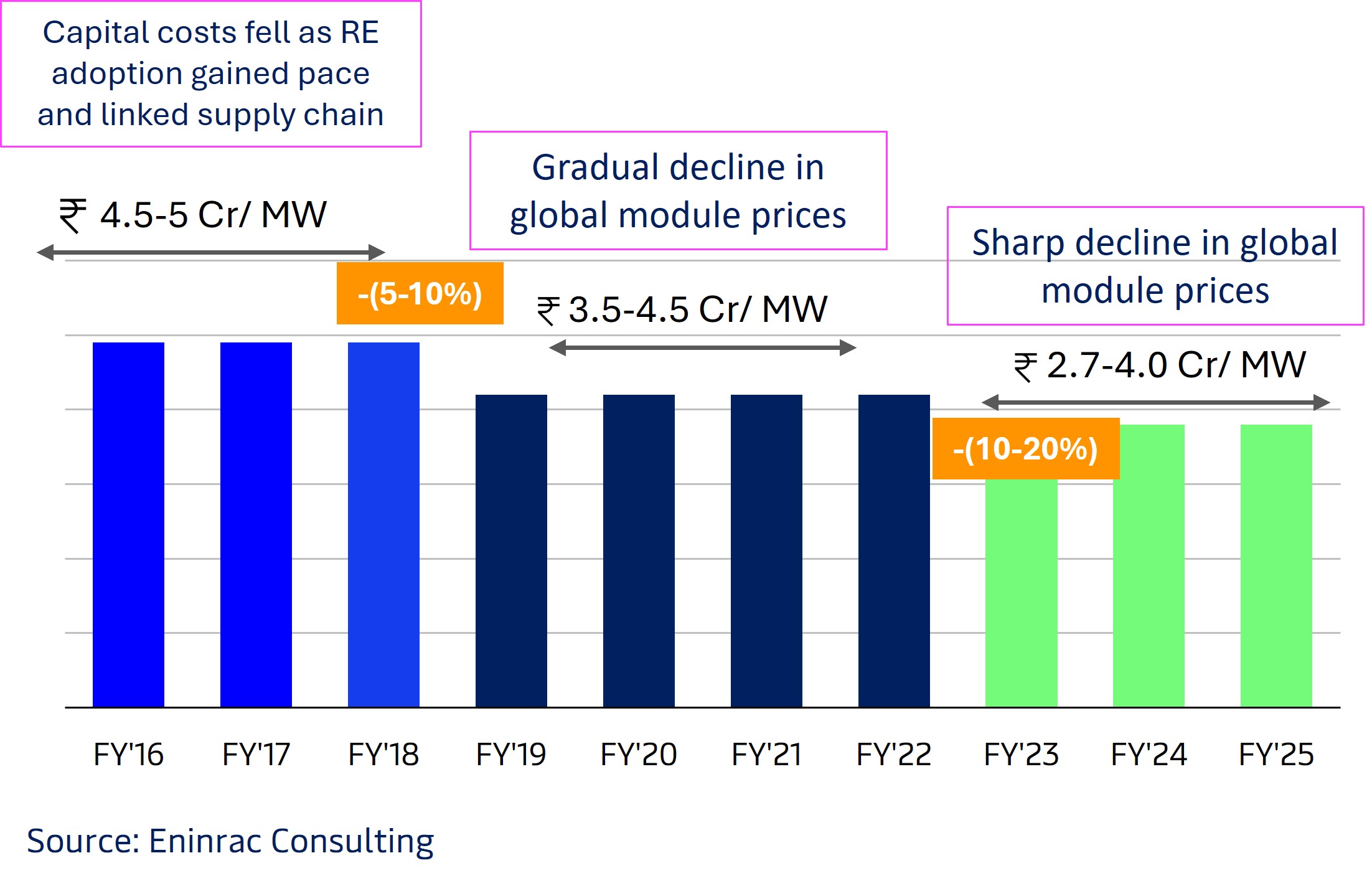

Capital costs for solar installations have seen a significant decline, from ₹4.5–5.0 Cr/MW in FY15–FY18 to ₹2.7–4.0 Cr/MW projected for FY24–FY25. This downward trend is driven by the global decline in module prices, advancements in manufacturing efficiency, economies of scale, and improved supply chain integration as renewable energy adoption accelerates.

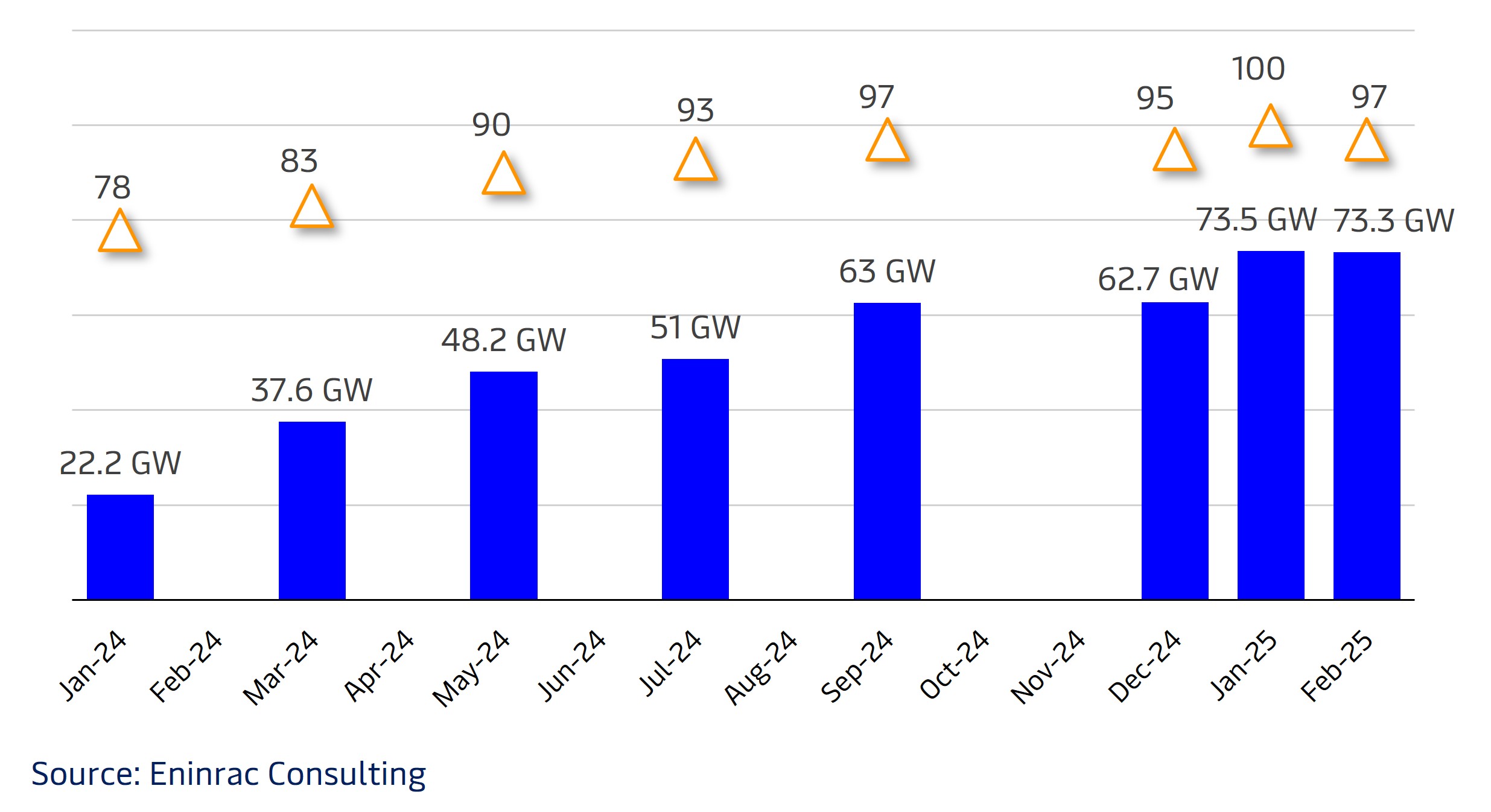

India’s ALMM enlisted capacity has grown steadily, reaching over 73 GW by February 2025. This growth reflects strong policy support, increasing manufacturer participation, and a maturing domestic solar ecosystem.

Declining Module Prices Leading to Lower Capital Costs

Technology Wise Share of PV Modules as of February 2025

India’s ALMM Enlistment Trend CY2024 – Feb 2025

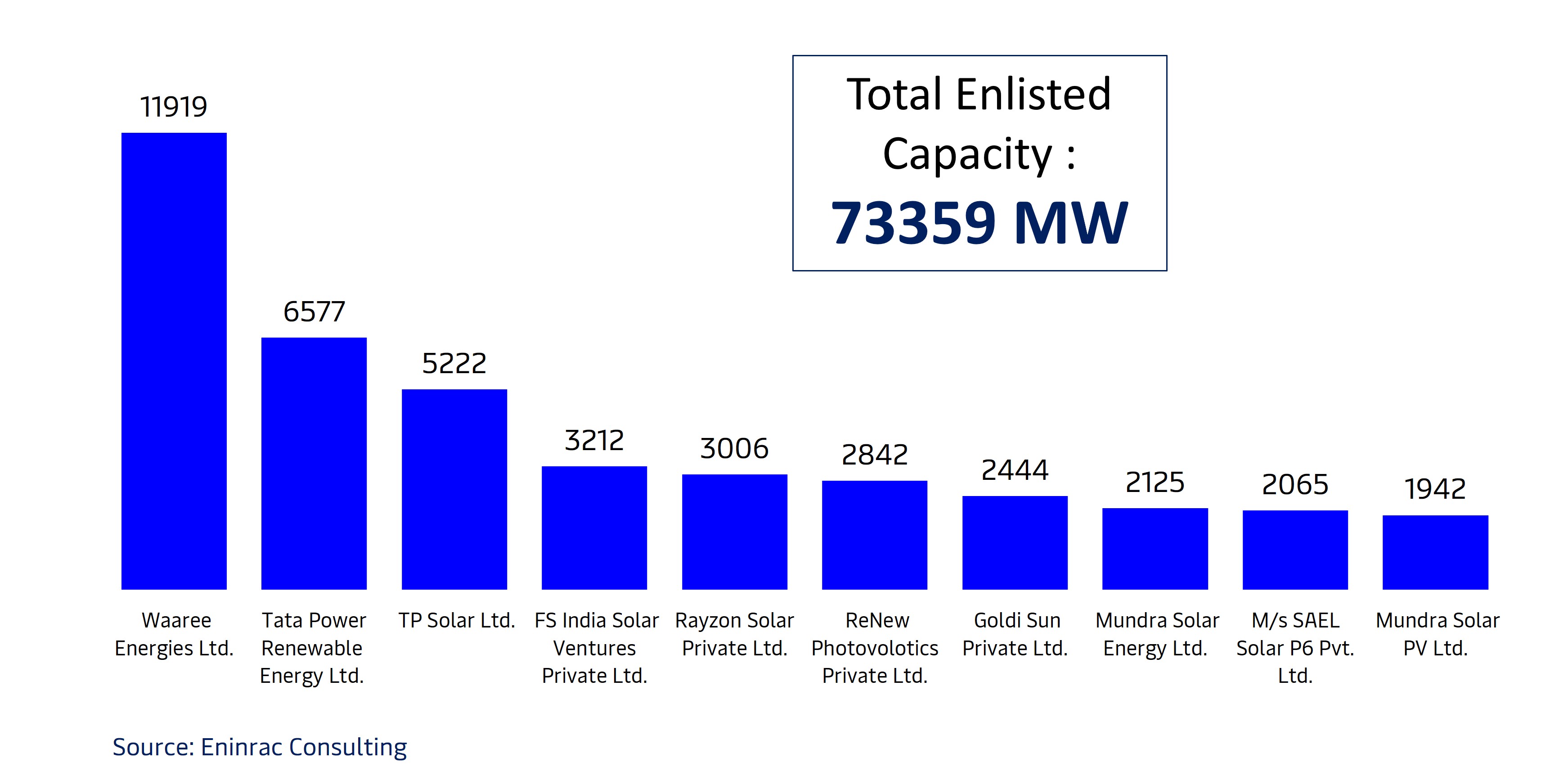

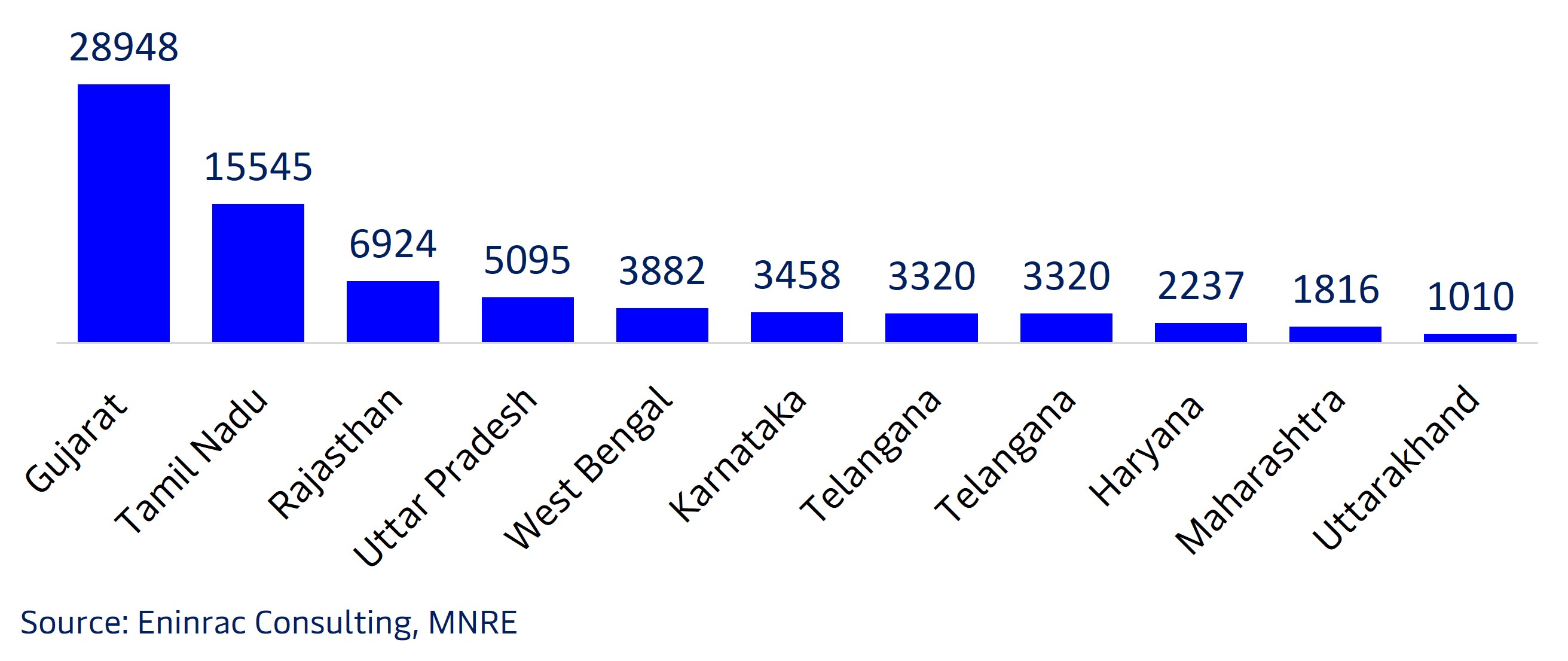

As of February 2025, India’s total enlisted solar PV module capacity stands at 73,359 MW, with major contributions from Waaree Energies Ltd. (11,919 MW), Tata Power Renewable Energy Ltd. (6,577 MW), and TP Solar Ltd. (5,222 MW). These top manufacturers underscore the consolidation of capacity among key players in the domestic module market. Gujarat leads among the states with the highest enlisted PV module capacity at 28,948 MW, followed by Tamil Nadu (15,545 MW) and Rajasthan (6,924 MW), reflecting strong policy frameworks, investment support, and infrastructure readiness in these regions.

Looking ahead, India's solar PV module manufacturing capacity is projected to grow at a CAGR of 10.46%, rising from 76 GW in FY2025 to 125 GW by FY2030. This growth is driven by strong government initiatives, rising domestic demand, and a push for self-reliance under programs like the PLI (Production Linked Incentive) scheme.

Leading Players Enlisted PV Module Capacity (MW) As of Feb 2025

Under India’s PLI Scheme for Solar Manufacturing, the government has significantly ramped up financial support to boost domestic capacity. The PLI outlay has increased from ₹4,500 Cr in 2021 to ₹19,500 Cr in 2022, and further to ₹24,000 Cr in 2025, underscoring a strong policy push toward self-reliance in solar manufacturing.

The PLI outlay has increased from ₹4,500 Cr in 2021 to ₹19,500 Cr in 2022, and further to ₹24,000 Cr in 2025, underscoring a strong policy push toward self-reliance in solar manufacturing.

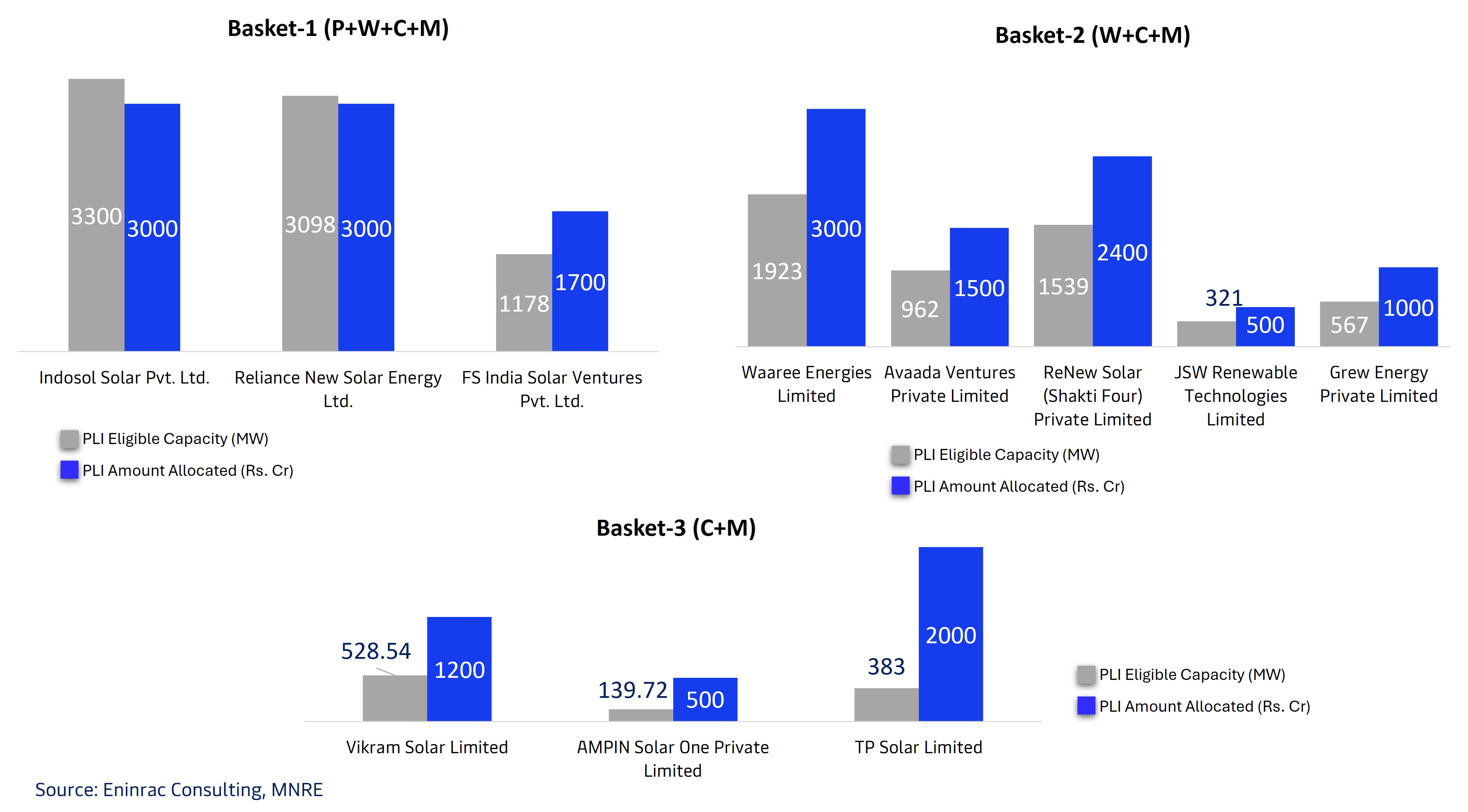

PLI Tranche II is categorized into three baskets:Basket-1 (P+W+C+M) includes full vertical integration, with top allocations to Indosol Solar Pvt. Ltd. (₹3,300 Cr), Reliance New Solar Energy Ltd. (₹3,098 Cr), and FS India Solar Ventures Pvt. Ltd.Basket-2 (W+C+M) supports partially integrated units, with Waaree Energies Ltd. receiving the highest allocation (₹1,923 Cr), followed by ReNew Solar (Shakti Four) Pvt. Ltd.Basket-3 (C+M) targets core manufacturing, with leading recipients including TP Solar Ltd. (₹383 Cr) and Vikram Solar Ltd. This initiative supports eligible capacity additions across different stages of the solar value chain, encouraging both scale and technology depth while reducing import dependency and promoting domestic innovation.

Leading States Solar PV Module Enlisted Capacity (MW) as of Feb 2025

PLI Tranche II- Status as of Mar’2025

Solar Manufacturing Investments

Key Corporate Bets

Reliance Industries is commissioning a 20 GW fully integrated solar giga-factory (modules, cells, wafers, ingots, polysilicon, glass) by end of FY2025-26. Waaree Energies operates 16.7 GWp of module and 5.4 GWp of cell capacity, with an additional 5.4 GW cell plant under construction in Gujarat. SAEL Solar is investing ₹82 billion (~US$929 million) in a 5 GW cell + 5 GW module facility in Uttar Pradesh.

Marquee Investment Announcements in 2025

Marquee Investment Announcements in 2025

Unlock the Full India Solar Manufacturing Market Report

We’ve shared a preview of the key insights. To receive the complete report (all slides, data tables, forecasts and analysis), simply click the button below, fill in a short form, and we’ll email the PDF to you instantly.