Analyzing the power demand- supply outlook across Indian states in the coming years, with a specific focus on the role of clean energy installations in shaping the energy landscape

-

How will India’s energy supply mix evolve by 2035, particularly the share of renewable & new energy sources?

-

How will advancements in energy storage technologies such as – BESS, PSP, green hydrogen shape India’s energy future by 2035?

-

What investments would be needed for grid expansion, smart grids and transmission networks to integrate clean energy sources ?

-

What should be India’s strategic pathway to 2035 for power demand-supply – roadmap & policy recommendations?

How will India’s energy supply mix evolve by 2035, particularly the share of renewable & new energy sources ?

How effectively can renewable energy and emerging technologies address India’s rising electricity demand by 2035 and what investment and market opportunities would unlock for value chain players – EPC, RE project developers, RE project developers, Green Hydrogen project developers, grid operators, OEMs, financial institutes etc. ?

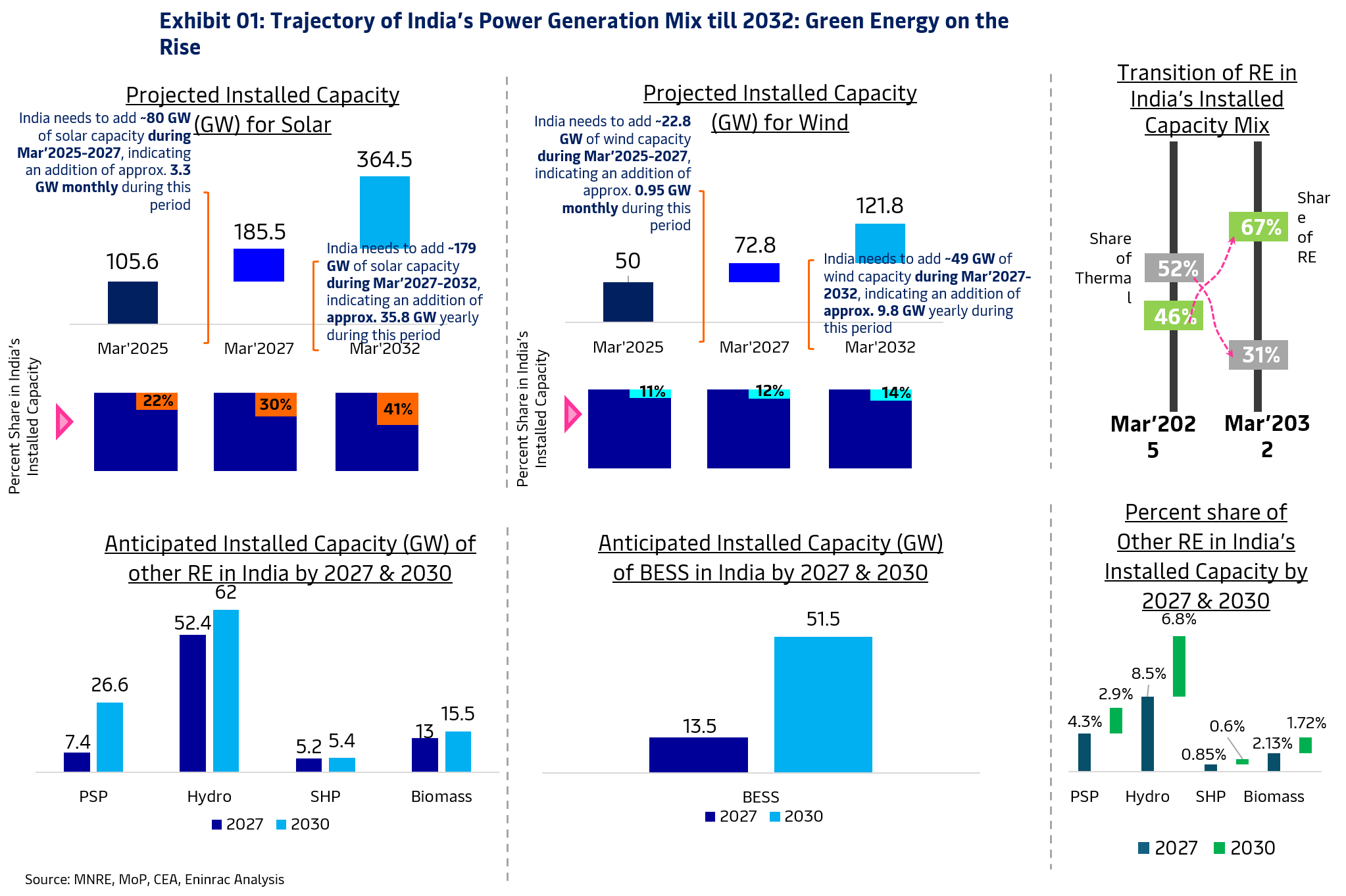

India’s energy supply mix is projected to undergo a significant transformation by 2035, with renewables

and new energy sources playing a dominant role. According to National Electricity Plan released in 2024-

the peak electricity demand in India is anticipated to grow by 11% from the current levels (Apr’2025)

and reach 277 GW by March’2027. Access the full report here:

To explore detailed forecasts, scenario analysis, and expert recommendations,

To meet the projected demand, the total installed power

generation

capacity is expected to reach 610 GW by March 2027, reflecting a growth of approximately 28%. Of this,

around 48%—equivalent to 284 GW—is anticipated to be contributed by renewable energy sources. As per

SECI/MNRE and plans by various States/UTs, additional renewable energy capacity is expected to be added

by March 2027.

To support round-the-clock power, this includes approximately 40 GW cumulatively

of

wind

and solar, along with battery energy storage systems (BESS), all of which have been considered for

transmission planning.

Opportunity for the Grid Operators

Green energy transition poses challenges as well as opportunities for the grid operators. Grid

integration of renewable energy involves navigating key challenges, that if approached innovatively,

could unlock new business opportunities.

The growing integration of renewable energy sources

(RES)

into

electric grids presents significant opportunities for investment and innovation. First, the increasing

need for grid infrastructure upgrades in high-potential renewable zones opens avenues for developing

advanced network expansion and optimization solutions. Second, the rising share of RES creates strong

demand for real-time monitoring and control technologies at the distribution level.

This

includes

solutions that enhance grid stability, ensure voltage and frequency consistency, and mitigate harmonic

distortion—critical for maintaining high reliability standards in modern power systems.

What expansion & investments would be needed for grid expansion, smart grids and transmission networks to integrate clean energy sources ?

To integrate the anticipated solar & wind capacity (both onshore & offshore) into the grid, the tentative cost requirement for commissioning the ISTS would be USD 28,729 Million approximately by 2030. For integrating standalone BESS, an investment requirement of USD 75 Million is anticipated by 2030. For modernization & strengthening of the power systems, India would require an investment of USD 425 Million by 2030.

The GEC Phase II, involves commissioning of 7577 ckt kms of intra state transmission lines to evacuate nearly 19 GW RE capacity. The total capital expenditure estimated for this is USD 1415 Million.

To cater to additional electricity demand on account of 10 million tonne per annum Green Hydrogen production by 2030, additional RE capacity would be required. It is estimated that the green hydrogen production would be close to major ports and end-use industries such as fertilizers, refineries, steel plants etc, hence requirement of supportive evacuation infra would required

Installed capacity of hydroelectric projects in the country is 46,850.18 GW (as on 31st October, 2022). Transmission system has been planned for about 16,673 MW additional hydro capacity likely to be commissioned by 2030.

Additional Inter-regional corridors by 2030. The present inter-regional transmission capacity is 112,250 MW. With the additional inter-regional corridors under implementation/planned, the inter-regional capacity is likely to be 149,850 MW in 2030

Additional HVDC corridors by 2030 The following HVDC corridors have been planned for integration of additional RE capacity by 2030: • ±800 kV Bhadla-III - Fatehpur HVDC line • ±350kV Pang - Kaithal HVDC line • ±800kV Barmer-II - Jabalpur HVDC line • ±800kV Khavda - Aurangabad HVDC line

What should be India’s strategic pathway to 2035 for power demand-supply – roadmap & policy recommendations?

Integrated grid modernization is definitely one such strategic pathway for India’s power demand-supply roadmap, supporting country’s energy transition plans.

Advancing Integrated Grid Planning for a Resilient and Future-Ready Power System

Current grid planning tools and methodologies are insufficient to effectively optimize existing capacity or strategically design new, efficient infrastructure. Traditional power flow models struggle to accommodate extended planning horizons and evolving uncertainties in both electricity demand growth (including load profiles) and supply characteristics (location, availability, dispatchability). These limitations hinder the ability to align with emerging regulatory frameworks. As a result, grid operators face significant challenges in modeling uncertainty across a diverse range of dynamic variables, including:

-

Distributed Energy Resource (DER) Forecasting: Anticipating the proliferation of electric vehicles, rooftop solar, and heat pumps to enable their seamless integration into the grid.

-

Climate Variability and Weather Patterns: Predicting the impact of intermittent renewable generation (e.g., wind and solar) and preparing for increasing frequency of extreme weather events to ensure grid resilience.

-

Asset Health and Reliability Modeling: Assessing the probability of infrastructure failure due to aging assets, vegetation encroachment, or environmental degradation, all of which influence operational reliability and long-term grid development.

Accelerating the renewable grid connection process by – Grid operators can optimize methodologies for hosting capacity estimation (for example, leveraging advanced grid planning models as described above); automate processes; leverage generative AI (gen AI) to improve customer interface and information flow; adapt connection requirements; standardize equipment; and ensure capital delivery excellence to accelerate the connection and permitting process.

Improving Operations– Grid operators can deploy advanced system stability and network adequacy technologies—such as smart inverters, prime movers, and virtual synchronous machines—while introducing innovative grid flexibility solutions like inertia procurement, congestion management services, and flexibility tenders. These measures help overcome physical infrastructure constraints, enhance grid resilience, and optimize real-time operational efficiency