India’s solar utility scale market offers a business case of US$ 200 Billion by 2032

This report — India’s Solar Utility-Scale Market Outlook till 2032, presents a value chain wise opportunity breakup of the $200 Billion market. It is the most comprehensive institutional-grade intelligence study available on this market. It spans 18 chapters, 250+ project-level data records, 28 state analyses and a full six-year forecast horizon across bull, base and bear scenarios. To unlock the detailed coverage, write to us at sales@eninrac.com

India stands at the most consequential inflection point in its energy history. Driven by binding

policy mandates, structural demand growth, rapidly declining technology costs and an

increasingly sophisticated project finance ecosystem, the country’s utility-scale solar sector

is transitioning from an emerging market opportunity to a fully institutionalized, large-scale

asset class commanding serious capital allocation from the world’s leading investment banks,

infrastructure funds, multilateral development banks and energy utilities.

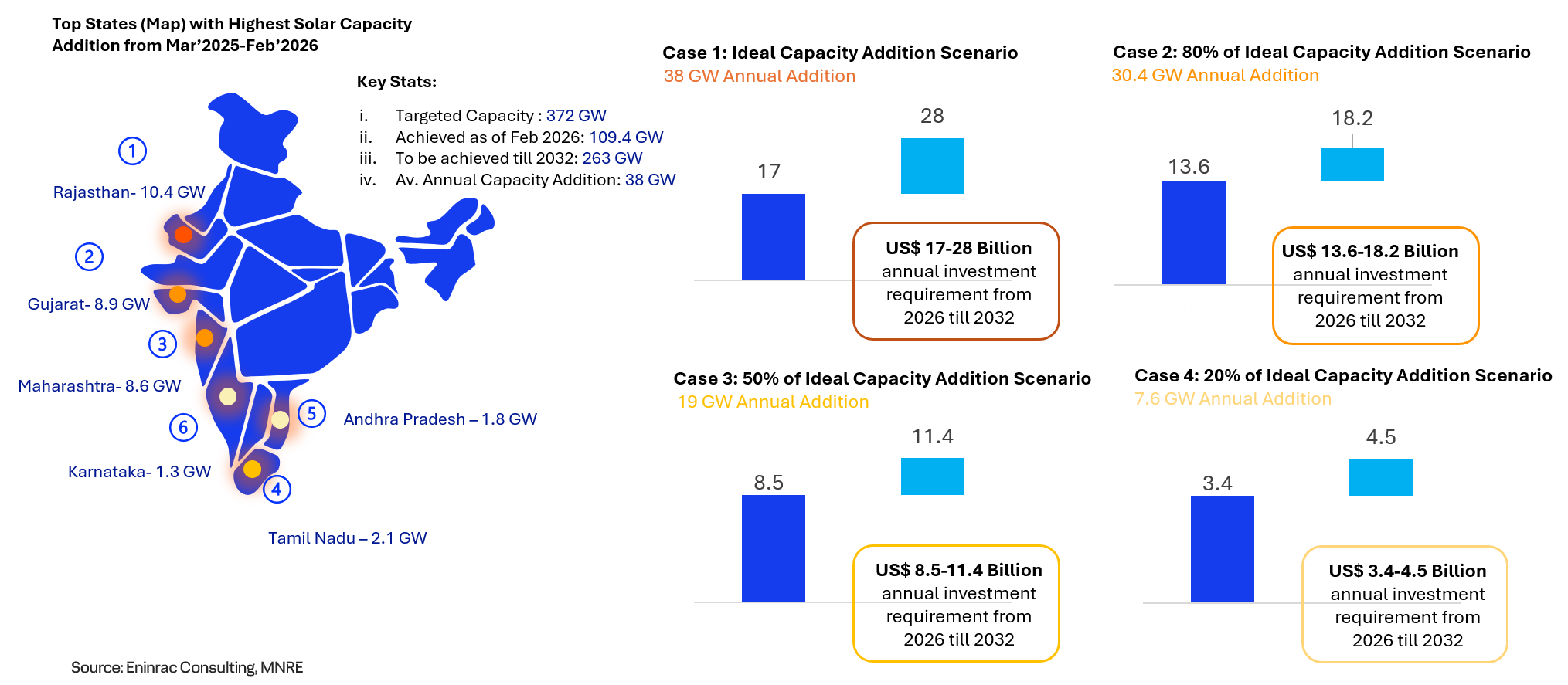

India must add approximately 38 GW of capacity annually till 2032 to meet its 372 GW solar

utility scale target. At a capital cost of US$ 550–650/kW, this translates to a total investment

requirement of US$ 144–171 billion over the period of 7 years— making Indian utility-scale solar

one of the largest infrastructure investment opportunities globally. With sovereign policy

backing, improving offtake credit frameworks, competitive tariffs, and a maturing project

finance market, the risk-adjusted return profile is now compelling for institutional capital at

scale.

India’s Strong Renewable Energy Policy Architecture that Positions it as a Key Hub for VC and PE Investments

India’s solar policy framework is now one of the most comprehensive in the world. The government’s National Solar Mission (NSM), anchored by the 500 GW renewable energy target under India’s Nationally Determined Contributions (NDCs) and the PANCHAMRIT climate commitments made at COP26, provides a clear, legally-backed demand signal through 2030 and beyond.

ALMM & BCD Framework: The Approved List of Models and Manufacturers (ALMM) and the 40% Basic Customs Duty (BCD) on imported solar modules have fundamentally reshaped India’s supply chain landscape, accelerating domestic manufacturing under the Production Linked Incentive (PLI) scheme. Over 65 GW of integrated wafer-to-module manufacturing capacity is being commissioned by 2026–2027, materially reducing India’s dependence on Chinese imports.

ISTS Waiver & RPO Mandates: The ongoing Inter-State Transmission System (ISTS) waiver for renewable energy projects — now extended through 2026 — continues to underpin the financial viability of large-scale solar projects. Renewable Purchase Obligations (RPOs) have been progressively raised, with the solar-specific RPO set at 40% by FY2030, creating a structural demand floor for solar power offtake

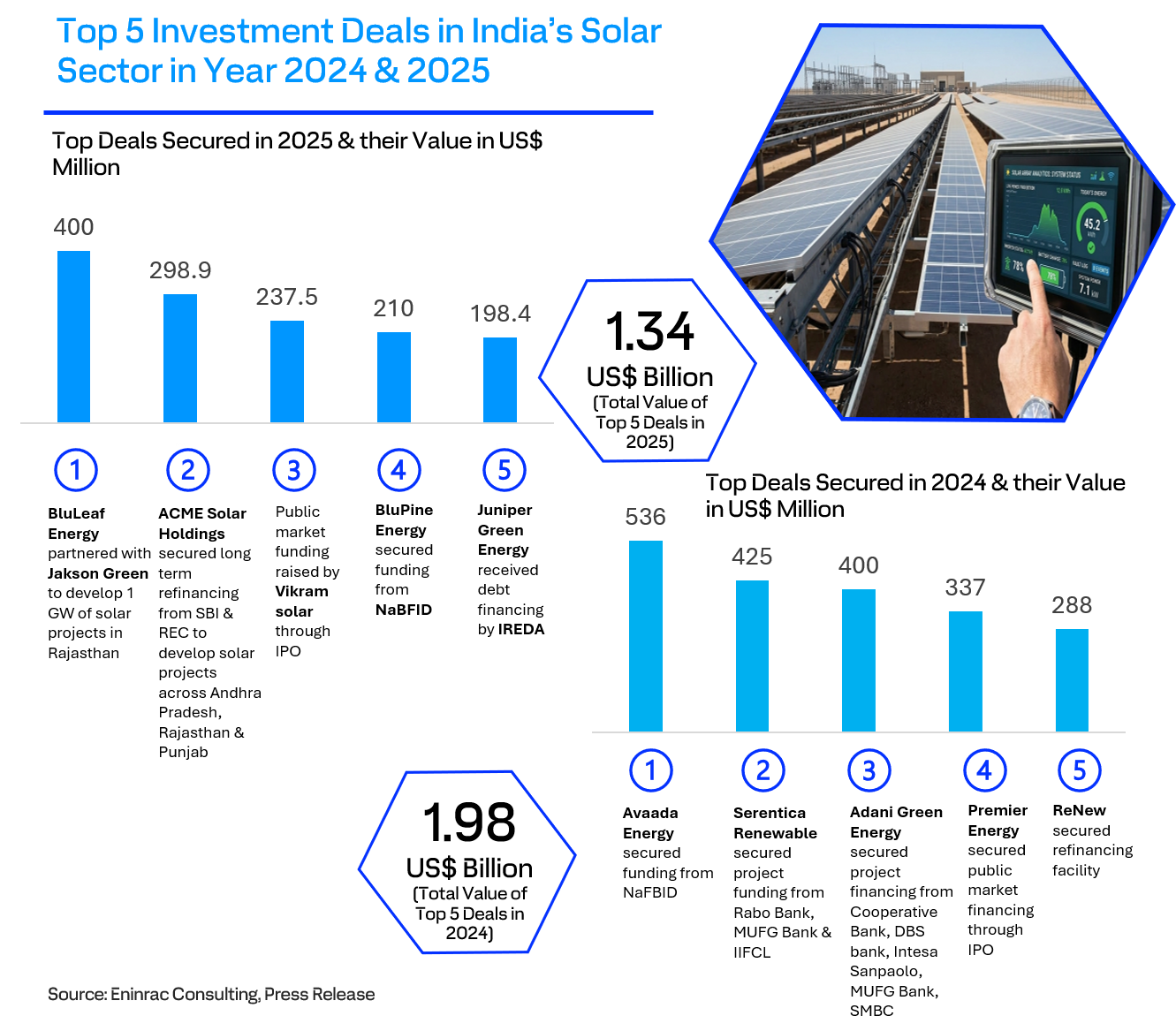

Exhibit 01 : Marquee Funding Deals/Partnerships in India’s Solar Sector during 2024 & 2025

Capacity Outlook: Annual Additions and Investment Requirements from 2026 to 2032

India’s installed utility-scale solar capacity stood at approximately 109.5 GW of the total solar installed capacity of 143.6 GW as of Feb 2026. The solar utility scale capacity is targeted to reach to 372 GW by 2031-32. To achieve this capacity, annually at least 38 GW of the capacity build up is required from a period 2026-2032.

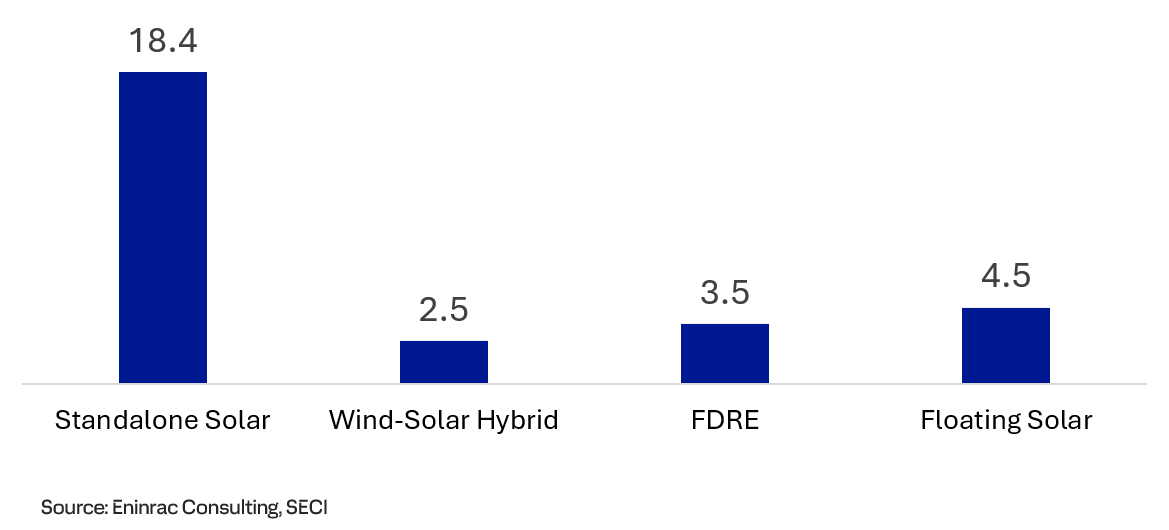

Rolled out Capacity: Solar Utility Scale Tenders by SECI from 2023 till Feb 2026

SECI rolled out nearly 18.4 GW of standalone solar PV tenders from 2023 till 2026. Additionally, 100 MW of floating solar tender, 2.8 GW of solar capacity under FDRE tenders and nearly 4 GW of wind solar hybrid tenders. All-in-all total 25.3 GW of RE tenders inclusive of solar utility scale has been rolled out from SECI during the period 2023-2026 (Jan).

Exhibit 02 : Anticipated Investment Requirement to Scale India’s Targeted Utility Scale Solar Capacity till 2032

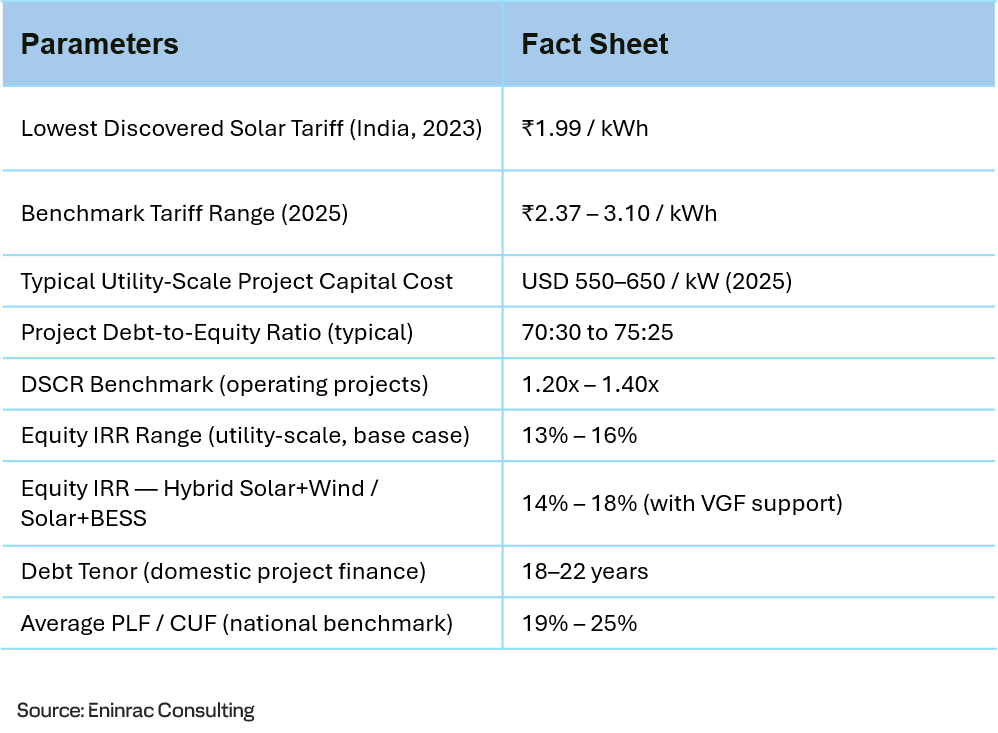

Tariff Economics & Project Returns: The Return Profile is Now Institutional Grade

Solar tariffs in India have declined by over 85% since 2010, reaching a historic low of ₹1.99/kWh in 2023 and stabilizing at ₹2.20–2.50/kWh in 2024–2025 following the impact of BCD and module cost increases. This floor-level tariff environment, combined with improving operational track records and declining project risks, has created a compelling risk-adjusted return profile for institutional investors

Exhibit 03 : Typical Tariff Economics & Project Returns for Solar Projects in India

Capital structure, financing landscape & investor ecosystem

India’s renewable energy project finance market has matured significantly, with a deep domestic banking system now actively supporting utility-scale solar through long-tenor rupee debt. State Bank of India (SBI), REC Limited, Power Finance Corporation (PFC) and Indian Renewable Energy Development Agency (IREDA) collectively account for over 60% of project debt to the sector. International financing from multilateral development banks (ADB, IFC, AIIB, World Bank), bilateral development finance institutions (JBIC, DEG, FMO, Proparco) and Export Credit Agencies (ECA) is providing catalytic capital, particularly for first-of-kind hybrid and storage projects.

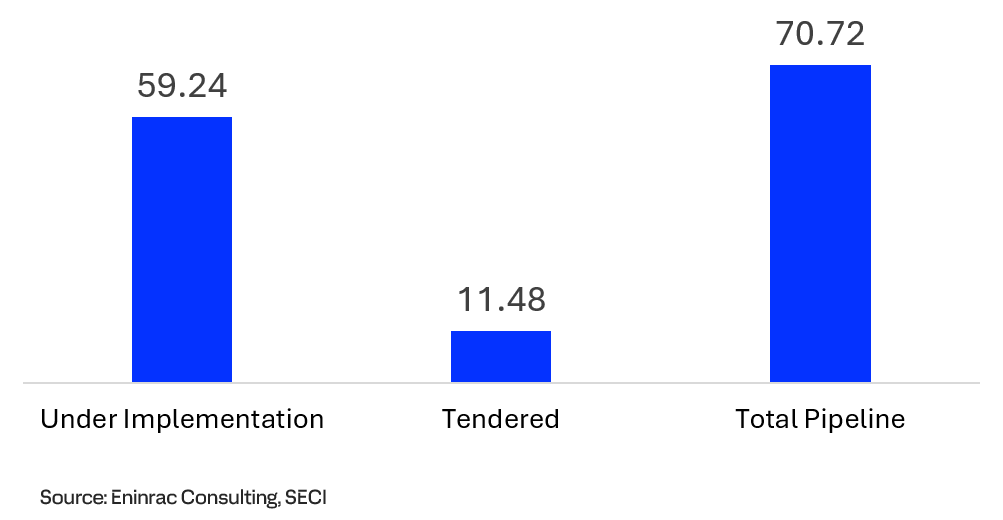

The Next Frontier: Round-the-Clock Renewable Power & Storage

The era of single-technology, peak-sunlight solar generation is giving way to a more sophisticated market structure defined by hybrid and dispatchable renewable power. India’s Round-the-Clock (RTC) renewable power procurement framework — requiring developers to supply firm, schedulable power — has catalyzed a USD 25–30 billion hybrid and storage investment wave that is reshaping project economics, technology selection and capital allocation strategies across the sector.

Exhibit 04 : Under Implementation Round-The-Clock/Hybrid/FDRE Projects (GW) in India

Exhibit 05 : Solar Utility Scale Capacity (GW) Tendered by SECI in India from 2023-Jan ’2026

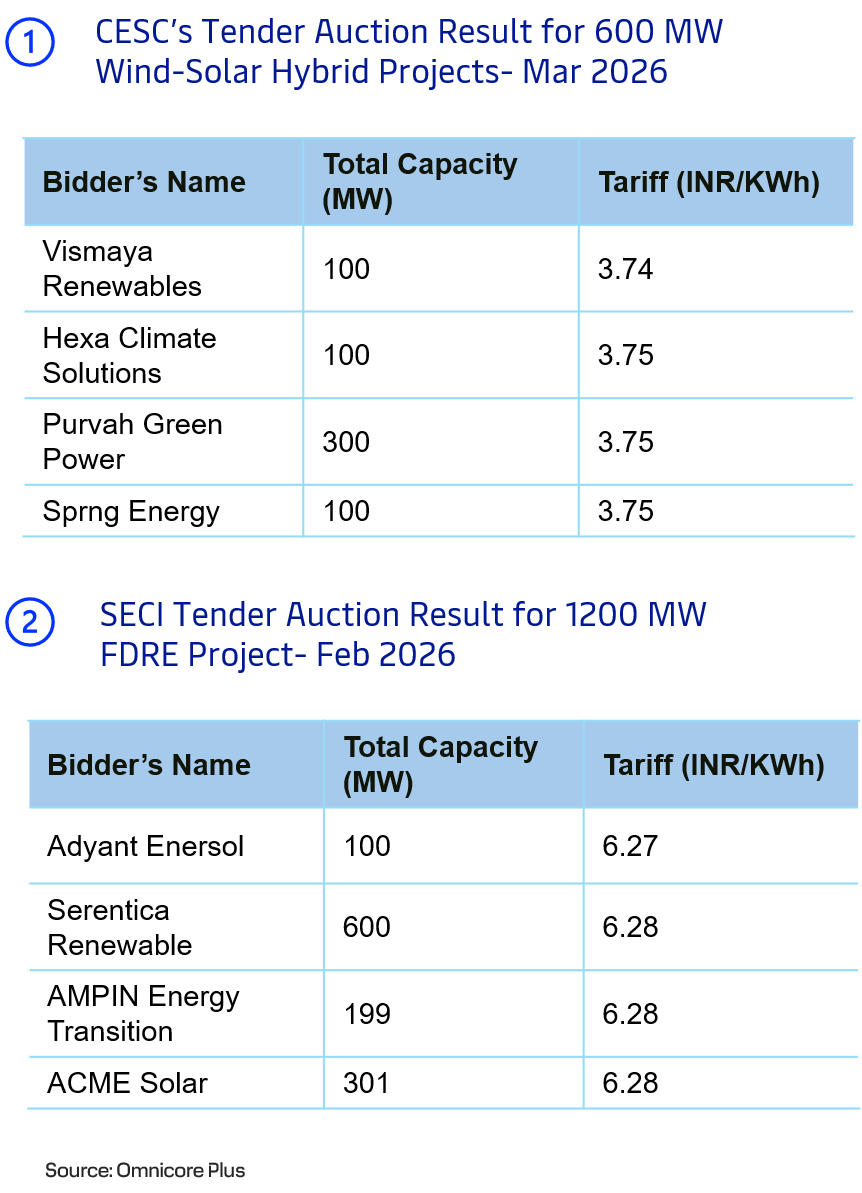

Exhibit 06: Latest Tender Auction Results for RTC/Hybrid/FDRE Projects in India

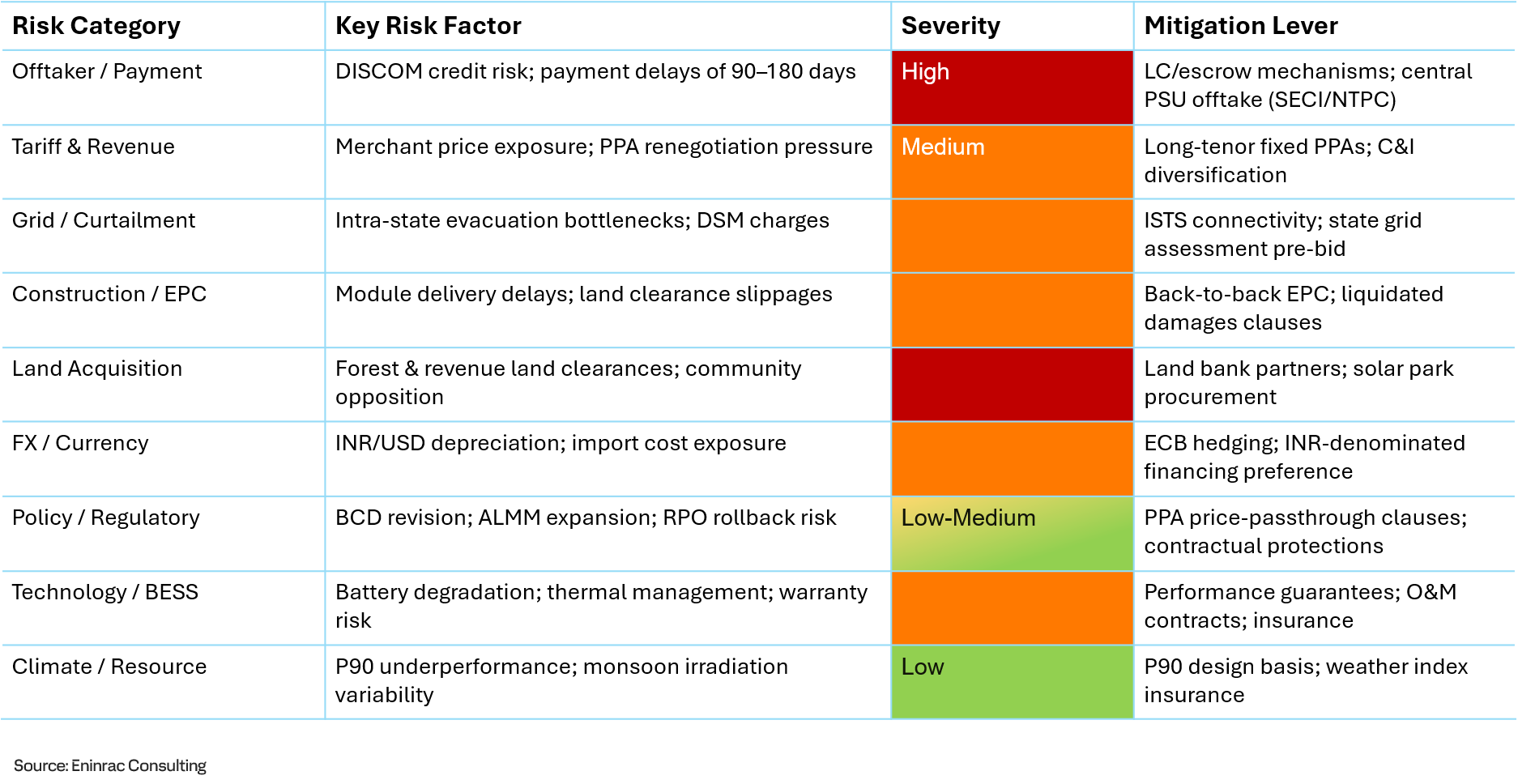

Structured Risk Assessment for Institutional Decision Making

India’s utility-scale solar sector offers compelling returns, but a rigorous understanding of its risk landscape is essential for institutional capital deployment. The following risk matrix captures the key exposures identified across this study’s 18 chapters and 250+ project records, together with the primary mitigation levers available to sophisticated investors

Exhibit 07 : Risk Assessment for Institutional Decision Making to Enter into India’s Solar Market