Draft National Electricity Policy India, 2026 - Observations & Comments by Eninrac Consulting Private limited

The Draft National Electricity Policy (NEP) 2026 outlines a strategic shift in market design, grid operations, and tariff frameworks aimed at supporting India’s energy transition while enhancing long-term economic competitiveness. The draft acknowledges enduring structural challenges, including financial stress in distribution utilities, distorted price signals, increasing system integration costs associated with variable renewable energy, and limited competitive intensity in power supply

Eninrac’s comments concentrate on specific regulatory measures where implementation risks, sequencing issues, or unintended consequences may undermine intended policy outcomes if not addressed at an early stage

The following sections outline the key regulatory actions proposed in the draft policy, evaluate their appropriateness, identify gaps and implementation challenges, and present Eninrac’s analytical insights and recommendations.

Against this global backdrop, India is steadily positioning itself as a key player in the semiconductor ecosystem. Supported by strong policy push, capital commitments, and initiatives aligned with the national vision of Make in India and Make for the World, the country is building both domestic capabilities and export-oriented capacity. Large-scale investments, expanding manufacturing infrastructure, and industry platforms such as SEMICON India 2025 reflect growing global confidence in India’s semiconductor ambition.

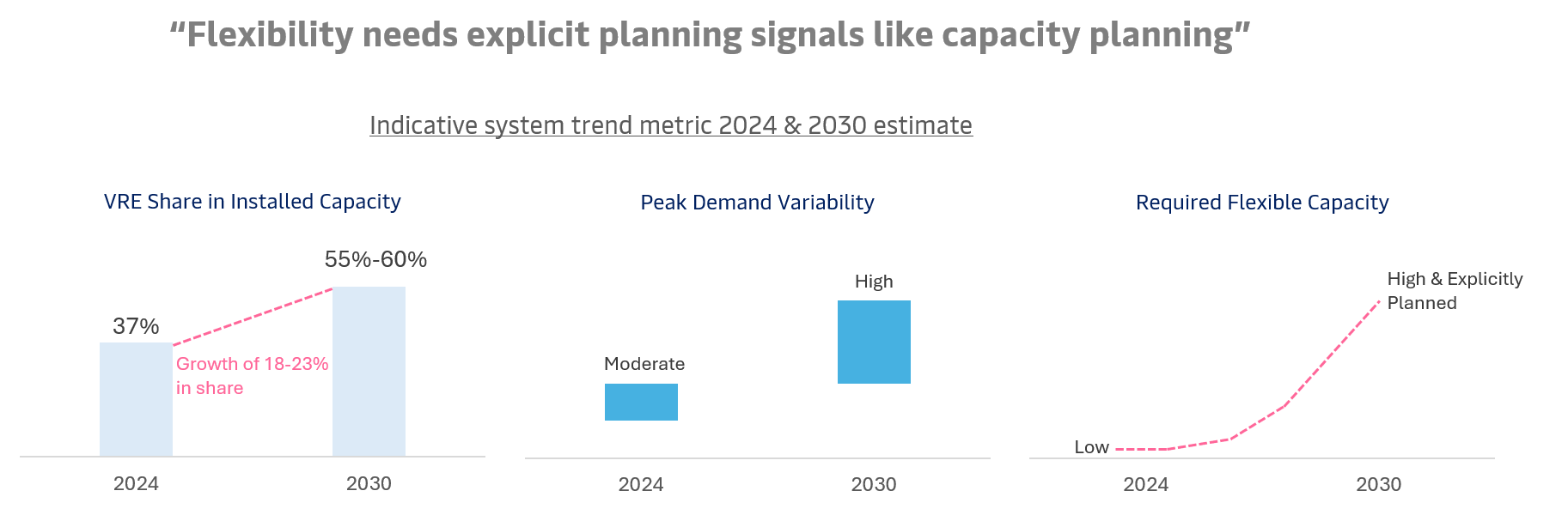

Flexible energy & grid structure

The draft promotes a flexible and resilient grid through large scale deployment of storage, hybrid renewable projects, ancillary services markets, aggregation of distributed resources, and advanced grid technologies. It emphasises flexibility from generation, storage, demand response, and transmission assets to manage rising demand.

The grid shifts from prevailing energy centric planning to flexibility centric planning w.r.t. dispatch relying on storage. Dispatch, balancing, and reliability increasingly rely on storage, flexible thermal assets, demand response, and market based ancillary services instead of fixed reserves.

Yes. With non fossil capacity expected to exceed 80% by 2047 and VRE already around 37% of installed capacity, flexibility becomes a facilitator that includes the generation capacity.

Flexibility is recognized conceptually but not quantified. There is no national or state level flexibility requirement metric. Ancillary service markets remain shallow and dominated by a few central generators. Distribution level flexibility and the role of DISCOMs as Distribution System Operators are under defined.

Eninrac recommends formal recognition of distributed energy as a regulated system asset with clear tariff recovery, and mandatory real time visibility of DERs through standardised data protocols.

Distributed energy & local grid optimization

The draft promotes distributed renewable energy, rooftop solar with storage, peer to peer trading, aggregators, and local RE plus storage by distribution licensees to reduce losses and transmission costs.

Energy production moves closer to load/load centres. Distribution networks evolve from passive carriers to active balancing platforms. Consumers become prosumers.

Yes. Distribution losses and congestion account for a material share of operational cost, especially in high demand urban and industrial clusters.

Commercial frameworks for aggregators remain undefined. Cost recovery for DISCOM owned distributed storage is unclear. Visibility of distributed resources at SLDC and DISCOM level remains weak.

“Distributed energy should be evaluated as a non-wired BESS alternative”

Eninrac recommends formal recognition of distributed energy as a regulated system asset with clear tariff recovery, and mandatory real time visibility of DERs through standardised data protocols

Distributed energy & local grid optimization

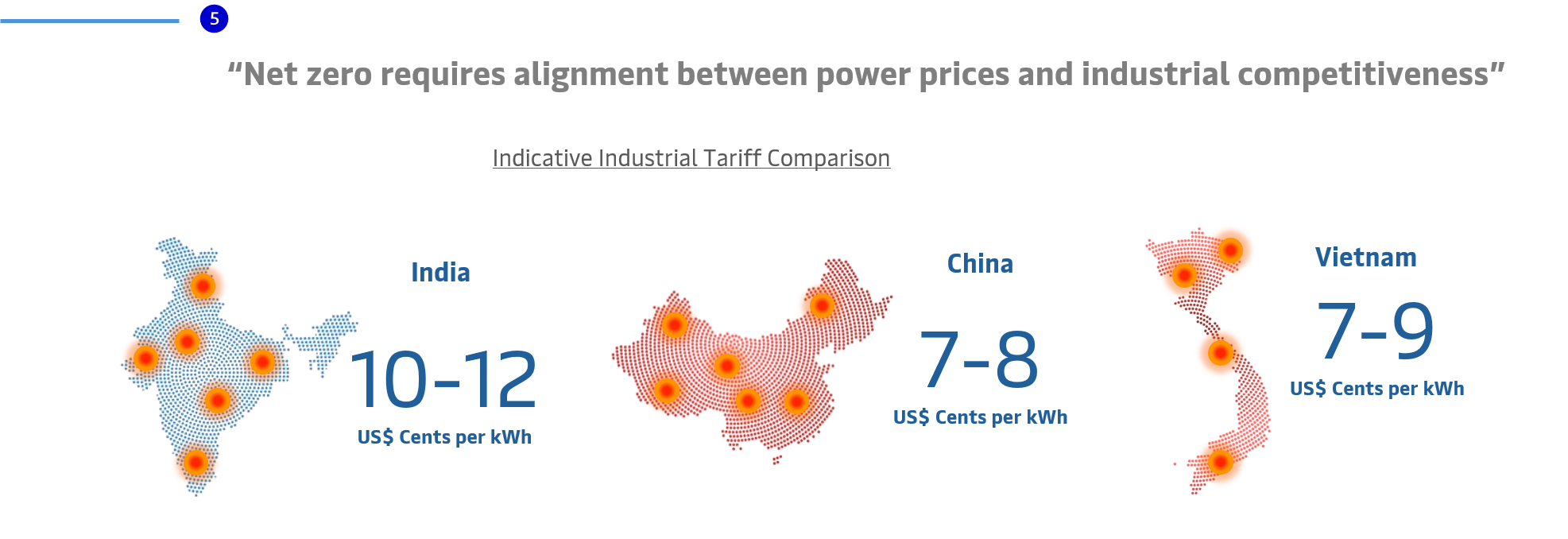

The policy aligns with net zero by 2070 through accelerated non fossil capacity, electrification of end use sectors, energy efficiency, and market based renewable procurement.

Electricity becomes the backbone of decarbonisation for industry, transport, and buildings. Power sector policy directly aligns with the net zero initiative to achieve national emissions trajectory.

Yes. India has already achieved over 50 percent non fossil capacity and surpassed earlier NDC targets ahead of schedule.

The policy lacks sector specific electricity demand trajectories linked to net zero pathways. Industrial decarbonisation relies heavily on high cost power due to cross subsidies.

Eninrac recommends aligning net-zero transition pathways with clearly defined power cost benchmarks for energy-intensive sectors, while prioritizing access to clean power for the manufacturing industry. Further, Eninrac proposes the establishment of a dedicated monitoring mechanism—anchored by an institution such as the Central Electricity Regulatory Commission (CERC)—to track and oversee the implementation of net-zero commitments for manufacturing sectors through the regulatory framework.

Unlock the Full India Draft National Electricity Policy India, 2026 – Observations

We’ve shared a preview of the key observations and insights from “Draft National Electricity Policy India, 2026 – Observations & Comments by Eninrac Consulting Private Limited. To receive the complete report (all slides, data tables, forecasts and analysis), simply click the button below, fill in a short form, and we’ll email the PDF to you instantly.