By 2030, India’s semiconductor market is targeted to reach a market value of US $ 100-110 Billion

By 2029, India is expected to develop the capability to design and manufacture semiconductor chips meeting approximately 70–75% of domestic application demand. By 2035, the country aims to establish itself among the leading global semiconductor nations. For a data-driven perspective on state-level competitiveness and region-wise manufacturing hub fitment, refer to Eninrac’s report, “Semiconductor Manufacturing in India: A $100 Billion Pathway,” featuring a structured indexation framework for investment decision support.

The global semiconductor industry is poised for unprecedented expansion, with companies worldwide planning investments of nearly USD 1 trillion in new fabrication plants (fabs) by 2030. Global annual industry revenues are also projected to exceed USD 1 trillion by the end of the decade, excluding the additional upside potential arising from the accelerated adoption of generative AI technologies. Beyond meeting rising demand, these large-scale investments are strengthening supply-chain resilience across the semiconductor value chain—an imperative underscored by recent global supply disruptions.

Over the past few years, semiconductor shortages disrupted production across sectors—from automobiles to consumer electronics—highlighting the strategic importance of chips to modern economies. In many ways, today’s digital world is built on semiconductors. With demand expected to grow significantly over the next decade, semiconductor design and manufacturing companies must undertake a comprehensive assessment of long-term demand drivers, technology transitions, and geopolitical realignments shaping the industry

Against this global backdrop, India is steadily positioning itself as a key player in the semiconductor ecosystem. Supported by strong policy push, capital commitments, and initiatives aligned with the national vision of Make in India and Make for the World, the country is building both domestic capabilities and export-oriented capacity. Large-scale investments, expanding manufacturing infrastructure, and industry platforms such as SEMICON India 2025 reflect growing global confidence in India’s semiconductor ambition.

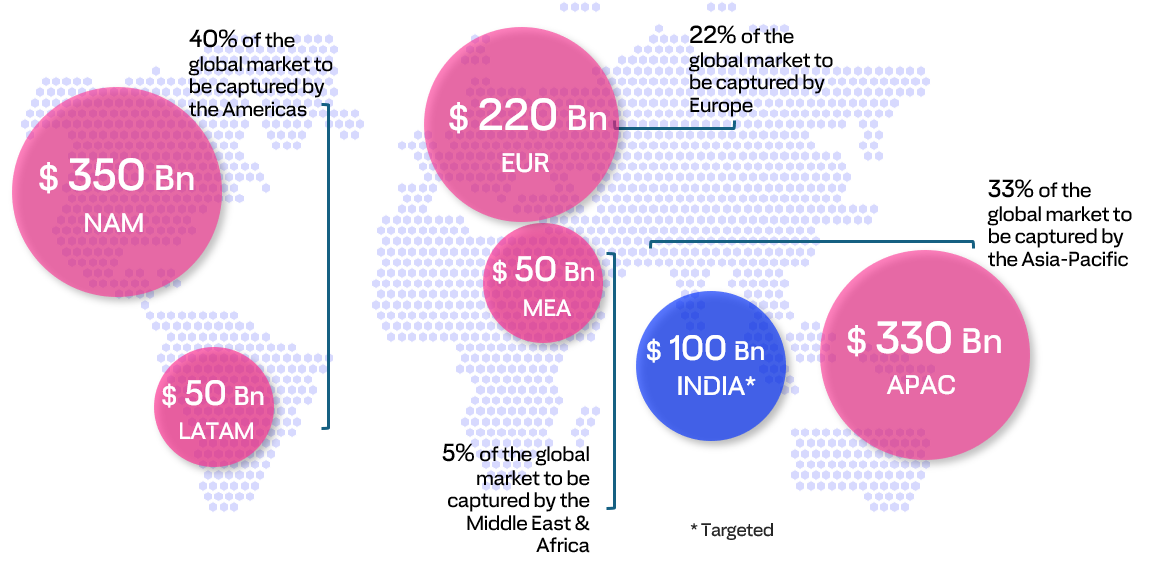

The Indian semiconductor market is witnessing robust growth. According to industry estimates, the domestic market was valued at approximately USD 38 billion in 2023, expanded to around USD 45–50 billion in 2024–25, and is targeted to reach USD 100–110 billion by 2030, boasting a size of 10% of global semiconductor market by 2030. Exhibit 01 indicates the anticipated market size of global semiconductors industry by 2030 for distinct international geographic regions. This rapid expansion positions India not only as a high-growth consumption market but also as an emerging manufacturing and design hub within the global semiconductor value chain.

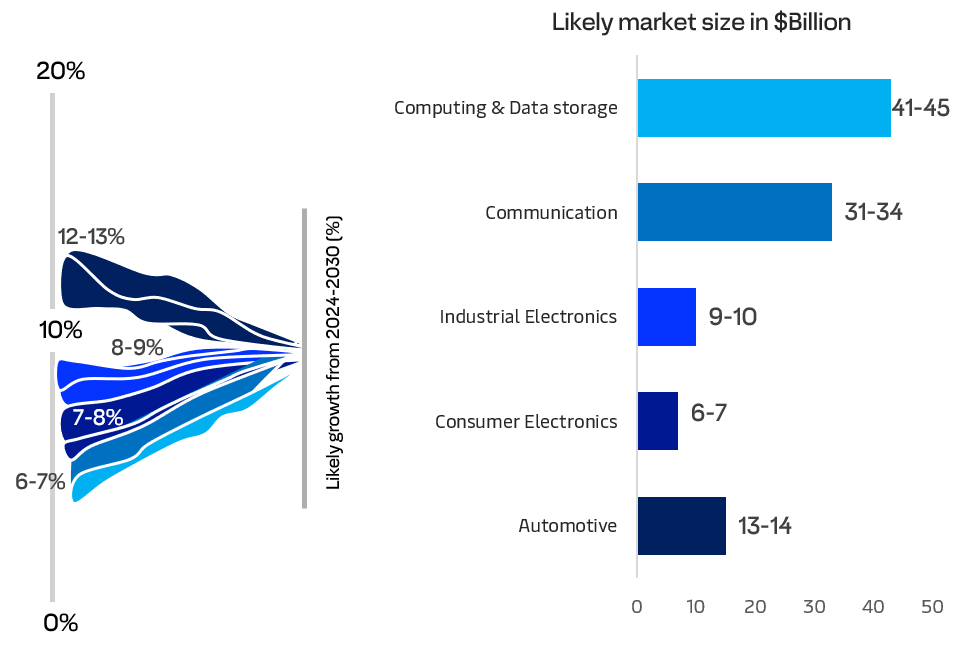

The overall growth in the semiconductor market in India would be driven by the automotive , data storage and communication segment and can be seen in Exhibit 02.

Exhibit 01 : Anticipated Semiconductor Market Size by 2030 for Distinct International Geographies

Source: Eninrac Consulting

Source: Eninrac ConsultingExhibit 02 : Anticipated Semiconductor Market Value in India by Industry Segments by 2030

Source: Eninrac Consulting

Source: Eninrac ConsultingApproved Semiconductor Manufacturing Projects in India as of Dec 2025

- Micron Technology Inc.

- Investment: INR 225.16 Bn

- Location: Gujarat

- Facility Type: Assembly & Testing of DRAM & NAND

- Production Capacity: 14 Million/week

- Tata Electronics Pvt Ltd

- Investment: INR 915.2 Bn

- Location: Gujarat

- Facility Type: FAB

- Technology Partner: PSMC Taiwan

- Production Capacity: 50,000 wafers/month

- Tata Electronics Pvt Ltd

- Investment: INR 271.2 Bn

- Location: Assam

- Facility Type: Semiconductor Packaging

- Production Capacity: 48 Million/day

- CG Power & Industrial Solutions Ltd

- Investment: INR 75.8 Bn

- Location: Gujarat

- Facility Type: Semiconductor Manufacturing

- Partnership: Renesas Electronics (USA), STARS Microelectronics (Thailand)

- Kaynes Technology India Ltd

- Investment: INR 33.07 Bn

- Location: Gujarat

- Facility Type: Semiconductor Chips

- Production Capacity: 6.33 Million/day

- Vama Sundari Investments Pvt Ltd

- Investment: INR 37.06 Bn

- Location: Uttar Pradesh

- Facility Type: Chips & Wafers

- Production Capacity: 20,000 wafers/month, 36 Million chips/month

- 3D Glass Solutions Inc.

- Investment: INR 19.43 Bn

- Location: Odisha

- Facility Type: Glass Panel Substrate, Assembly & 3DHI

- Production Capacity: 5,800 panels/month, 4.20 Million units/month assembled, 1,100 units/month for 3DHI

- SiCsem Pvt Ltd

- Investment: INR 20.66 Bn

- Location: Odisha

- Facility Type: Wafers & Packaging

- Production Capacity: 5,000 wafers/month, 8 Million packaging units/month

- Continental Device India Pvt Ltd

- Investment: INR 1.17 Bn

- Location: Punjab

- Facility Type: High Power Discrete Semiconductor Devices

- Production Capacity: 158.38 Million units/annum

- Advanced System in Packaged Technologies Pvt Ltd

- Investment: INR 4.8 Bn

- Location: Andhra Pradesh

- Facility Type: Semiconductor Manufacturing

- Production Capacity: 96 Million units/month

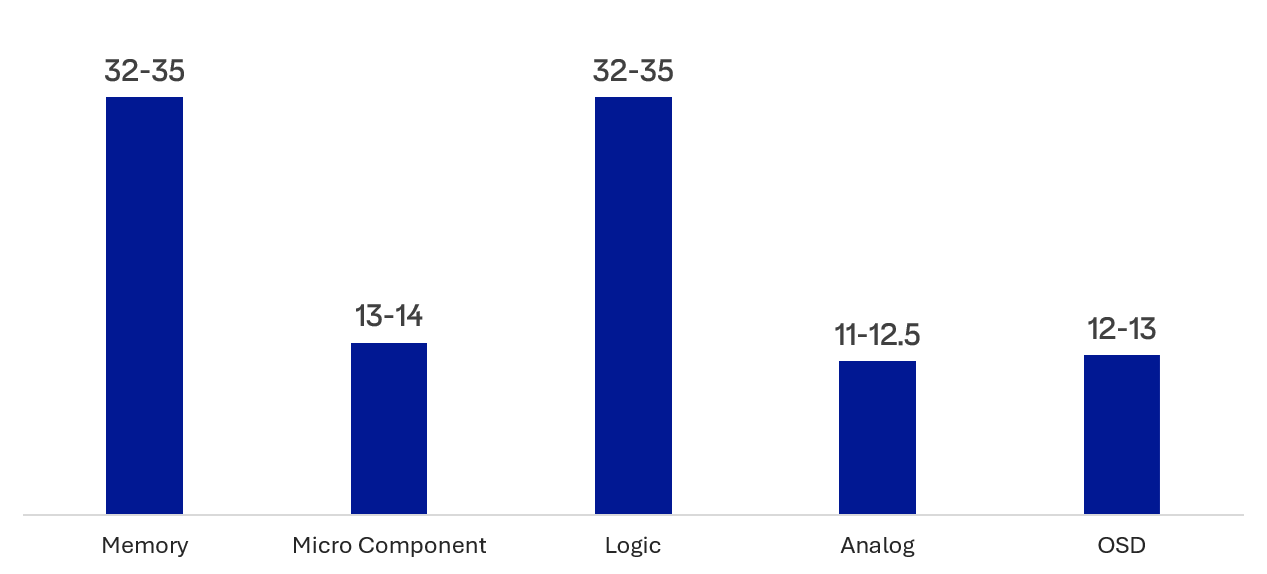

Exhibit 03 : Anticipated Semiconductor Market Value in India by Component Type by 2030 in US$ Billion

Source: Eninrac Consulting

Source: Eninrac ConsultingThe market participants in India's semiconductor industry will need to tame these barriers and convert them into a strategic edge and first mover advantage to fully realize the benefits from announced investments and others that may come.

-

1. Barrier: High Greenfield Capital Expenditure (CapEx)

Strategic Edge: First-Mover Infrastructure Control

Instead of viewing the high cost of building new infrastructure as a burden, first movers can build captive, green energy-powered fabs with dedicated power and water plants. This creates energy independence and insulates them from future grid volatility, turning a cost disadvantage into a reliability advantage that latecomers cannot easily replicate.

-

2. Barrier: Lack of a "Fab-Ready" Skilled Workforce

Strategic Edge: Proprietary Talent Pipeline

By establishing the first industry-led training academies and university partnerships, a first mover can capture India’s demographic dividend. They secure top engineering talent at a 30–40% cost advantage while building a loyal, specialized workforce, creating a long-term competitive moat.

-

3. Barrier: Dependence on Raw material imports

Strategic Edge: Captive Materials Production

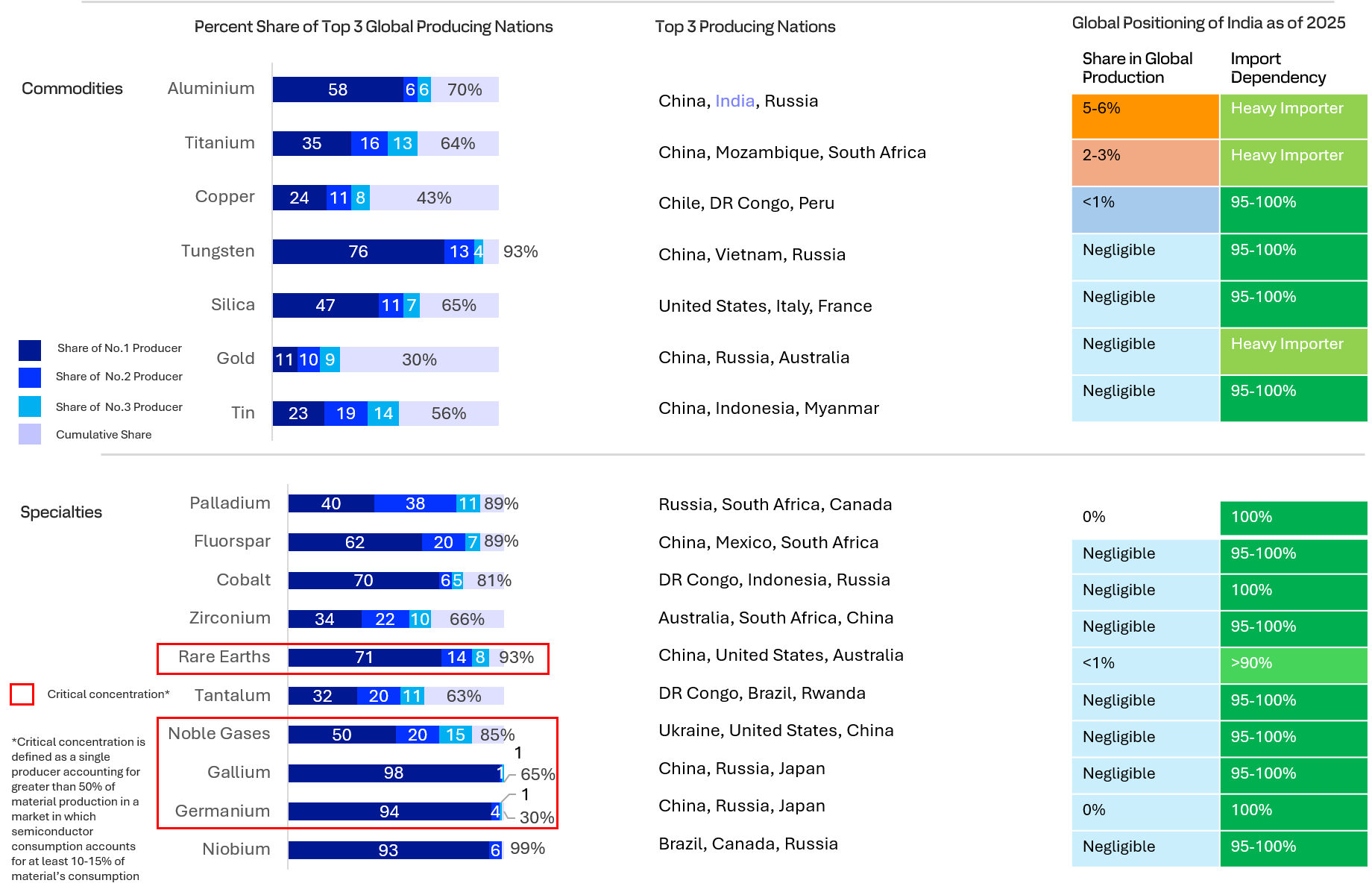

First movers can partner with global leaders to co-locate specialty chemical and gas plants within their fab ecosystems. This vertical integration slashes logistics costs and lead times, turning a supply chain vulnerability into a cost advantage and insulating the player from global export controls. India’s global positioning in the raw material supplies for semiconductors can be seen in Exhibit 06. India possesses a significant, yet under-leveraged, position in the global raw material supply chain for semiconductors, how India can overcome this barrier in due course of time & what possible could be the strategic implications for the early market birds can be seen in Exhibit 07.

-

4. Barrier: Multi-Year Qualification Cycles for New Materials

Strategic Edge: De Facto Market Standards

Early players who qualify locally sourced materials first control qualification data and effectively set industry standards, creating strong customer lock-in and raising entry barriers for latecomers.

-

5. Barrier: Concentration of Advanced Packaging in East Asia

Strategic Edge: Integrated OSAT + Materials Hub

By building backward-integrated OSAT facilities with local substrate and lead-frame production, first movers can offer faster delivery and lower total costs for Indian customers.

-

6. Barrier: Immature Logistics & Specialized Handling Infrastructure

Strategic Edge: Ownership of the Logistics Chokepoint

Investing in dedicated semiconductor cargo terminals and controlled handling facilities enables first movers to create mandatory gateways, monetizing logistics infrastructure as a strategic asset.

-

7. Barrier: Long Lead Times for Critical Spares & Consumables

Strategic Edge: "Inventory-as-a-Service" Hub

First movers can build bonded warehouses for high-risk, long-lead items. As the ecosystem grows, they can offer this buffer stock as a service to smaller fabs and OSATs, transforming a cost center into a regional profit center and becoming the critical "parts depot" for the entire Indian industry.

Exhibit 04 : The Regionalization Imperative: 5 Material Segments that could lead to Logistical Success of Semiconductor FAB in India

| Material Segment | Why Regionalization is Critical in India | Strategic Advantage for First Movers |

|---|---|---|

| Bulk & Specialty Gases (Nitrogen, NF₃, WF₆) |

Fabs consume gases continuously; cryogenic transport over Indian highways is risky, costly, and prone to monsoon disruptions. Hazardous nature requires strict compliance. |

On-Site Sovereignty: Build captive generation plants or pipeline networks. Guarantee 100% uptime while insulating operations from future price volatility and import licensing delays. |

| Wet Chemicals & CMP Slurries |

High purity degrades rapidly in Indian climate (heat, humidity). Long transit times from ports increase contamination risk and reduce bath life in fabs. |

Quality Lock-In: Establish local blending and purification hubs. Deliver "fresh" chemicals with extended life, reducing fab costs and ensuring process consistency that import-dependent competitors cannot match. |

| Packaging Substrates & Lead Frames |

Bulky, custom, and supply-constrained globally. India's OSAT ambitions require localized production to cut logistics costs and lead times for domestic automotive and electronics customers. |

Integrated Ecosystem: Build adjacent substrate manufacturing to serve your own OSAT. Slash customer lead times from months to weeks, capturing the "China Plus One" premium. |

| Precursors & Photoresists |

Ultra-high value, short shelf life, often pyrophoric or toxic. Import dependence creates vulnerability to global supply shocks and customs delays. |

Resilience Hub: Establish bonded, cold-chain warehouses with consignment stock. Offer "just-in-time" delivery to multiple fabs, becoming the critical regional supply node. |

| MRO Spares & Consumables (Quartzware, Pumps, Parts) |

Fab downtime costs exceed $100,000 per hour. Air-freighting spares from East Asia takes 3-5 days—too long for critical failures. |

Downtime Prevention: Build the first regional MRO hub with consignment inventory. Guarantee 4-hour response times, turning logistics into a customer acquisition tool for fab services. |

-

8. Barrier: Unpredictable Import Licensing (e.g., for high-silver materials)

Strategic Edge: Regulatory Fast-Track Partnership

First movers can collaborate with the Indian government to establish end-use certification systems and green-channel clearance for bona fide manufacturers, turning bureaucratic hurdles into relationship-based strategic advantages.

-

9. Barrier: Opaque Global Supply Chains & Disruption Vulnerability

Strategic Edge: Predictive Supply Chain Intelligence

Early movers can deploy digital twin technologies to map their supply chains, predict geopolitical or weather-related disruptions, and activate alternative sourcing strategies before competitors.

-

10. Barrier: High Energy Costs & Volatility

Strategic Edge: Renewable Energy Sovereignty

By signing long-term renewable power agreements and integrating battery storage, first movers can lock in predictable, low-cost green energy, transforming volatile operating expenses into durable competitive advantage.

-

11. Barrier: Complexity of Location Fitment Analysis Across Competing States

Strategic Edge: Location Arbitrage through Ecosystem Lock-In

First movers can conduct data-driven state selection based on power, water, logistics, and seismic stability, negotiate exclusive incentive packages, and shape local talent pipelines—creating a durable geographic moat.

Exhibit 05: Critical Raw Materials are Concentrated Among a Few Subtier Component Supplier

India's Critical Raw Material Advantage & Strategic Implications

| Critical Material | India’s Position | Strategic Implications |

|---|---|---|

| Quartz & High-Purity Silica |

India has abundant deposits of quartzite, a primary raw material for crucibles and quartzware used in crystal pulling furnaces. |

First movers can establish local quartz crushing, beneficiation, and crucible manufacturing units, reducing dependence on imports from Russia and the US |

| Rare Earth Elements (Lanthanum, Cerium, Neodymium) |

India possesses ~6% of global rare earth reserves, with significant monazite deposits in coastal sands (Andhra Pradesh, Tamil Nadu, Odisha). Used in CMP slurries, phosphors, and specialty glasses. |

Local processing and separation facilities can create a domestic supply chain for rare earth-based semiconductor materials, reducing China's dominance. |

| Copper & Base Metals |

India is a major copper producer; high-purity copper is essential for lead frames, bonding wires, and interconnects. |

Local refining to semiconductor-grade purity (99.99%+) can support OSAT and packaging units with reduced import lead times. |

| Specialty Gases (Argon, Helium) |

India has growing air separation capacity for argon. Helium, though limited, can be extracted from specific natural gas fields with appropriate investment. |

On-site or regional air separation units can supply bulk gases, while helium recovery and recycling systems reduce import dependency. |

| Gallium & Indium |

India has bauxite reserves containing gallium and zinc reserves containing indium—both critical for compound semiconductors (GaAs, GaN, ITO). |

Establishing recovery and refining capabilities positions India as a supplier for downstream compound semiconductor fabs. |