India has been a hotspot of developing datacenters across the globe and is likely to add on the data centers massively in coming years, given the demand spurt and rising concerns of cyber security. As the number of datacenters grow the requirement of their automation would follow in-suit which pushed the assessment of market opportunity for a global major as per different tiers & storage requirement, datacenter inventory, vacancy, under construction and planned status etc. in order to clearly understand the gap in demand-supply of automation market in the country for datacenters

DATA CENTER - It is the facility that centralizes an organization’s IT operations and equipment, where it stores, manages and disseminates data. These may physical or virtual repositories of the network’s most critical systems, ensuring the proper uninterrupted functioning of the network.

In considering their functions, as in most more developed economies, data centers in India serve a wide range of sectors & industries from internet, including Government, manufacturing, education, media, e-commerce, energy, transportation & logistics, finance, medical & healthcare and others. Although, each data centre is unique in design, they can be generally be classified based on flowing:

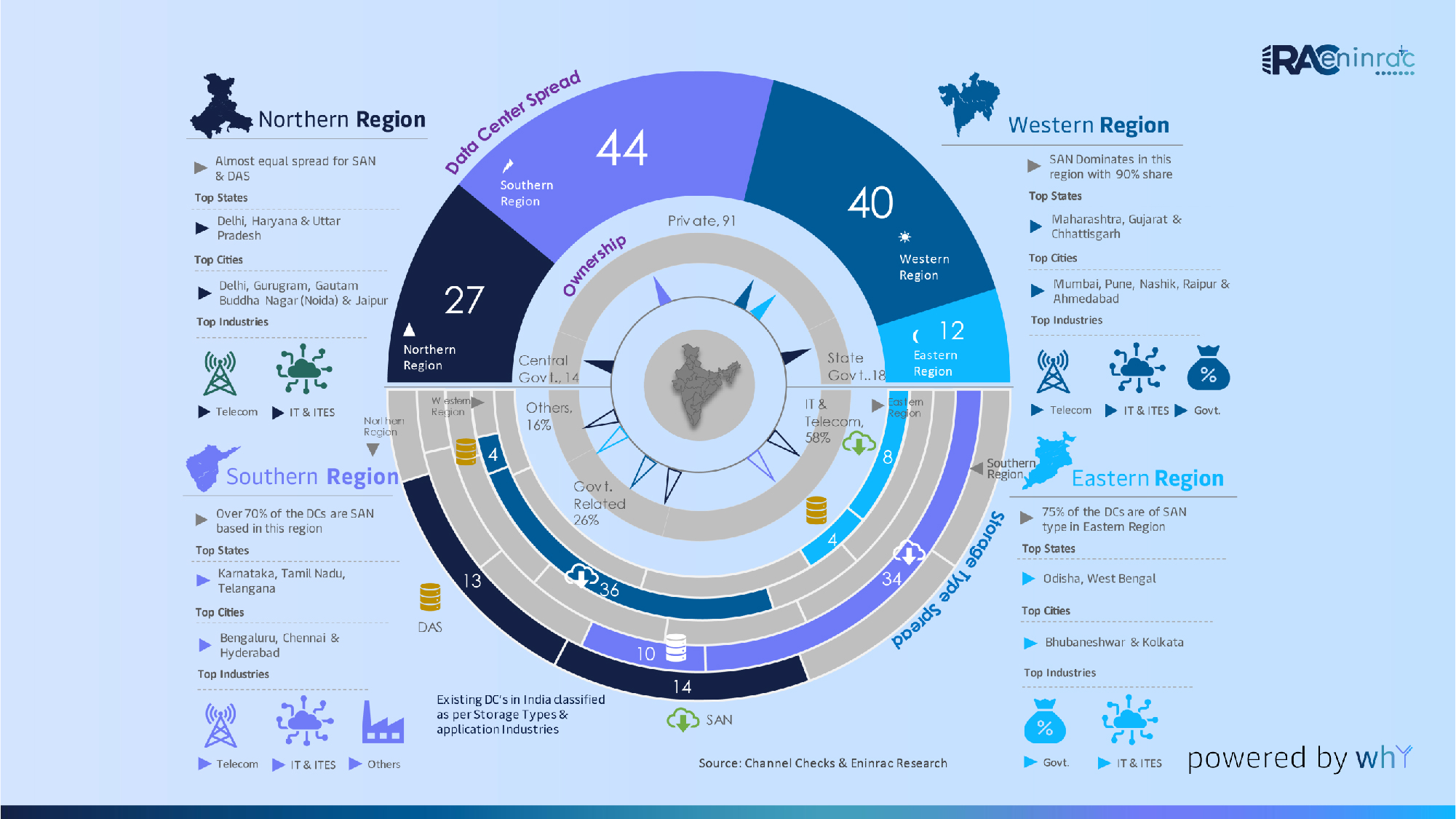

BY LOCATION - DC is classified as to where they are located, either as internet-facing (cloud-based) or captive (in-house data centers).

DC are classified as per their ownership as well as Government Managed or State-Owned Enterprise (SOE) Managed or Privately Managed

DC is also classified as per energy use. The range of use varies from a few kW (kilowatts) to tens of thousands of kW. We have categorized this as per our intense primary research of existing data centers in India and are indicated as below:

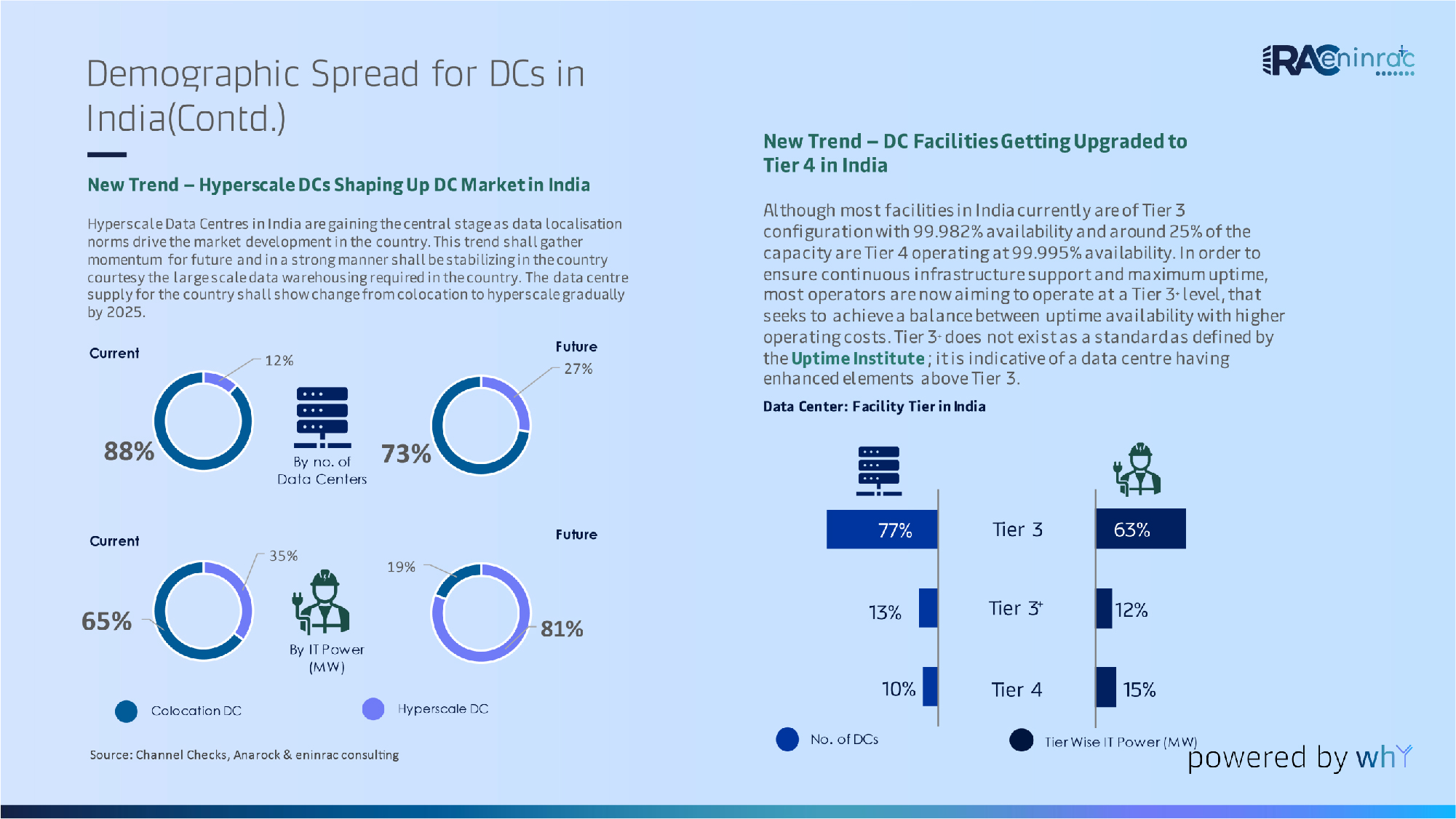

The availability is based upon a rating designed by Uptime Institute Tier rating, which is used to classify data centers the basis on standards for minimum uptime and maximum uptime. The classification is detailed as well:

Do you want to seek Eninrac assistance in helping you resolve some critical business issues? Engage with us and reach out to our experts by using the Request for Proposal (RFP) form.

Complete the form to connect with our sales team and see the Visionboard platform in action. Discover how Eninrac helps your teams eliminate poor market research experiences and drive actionable insights.